.png)

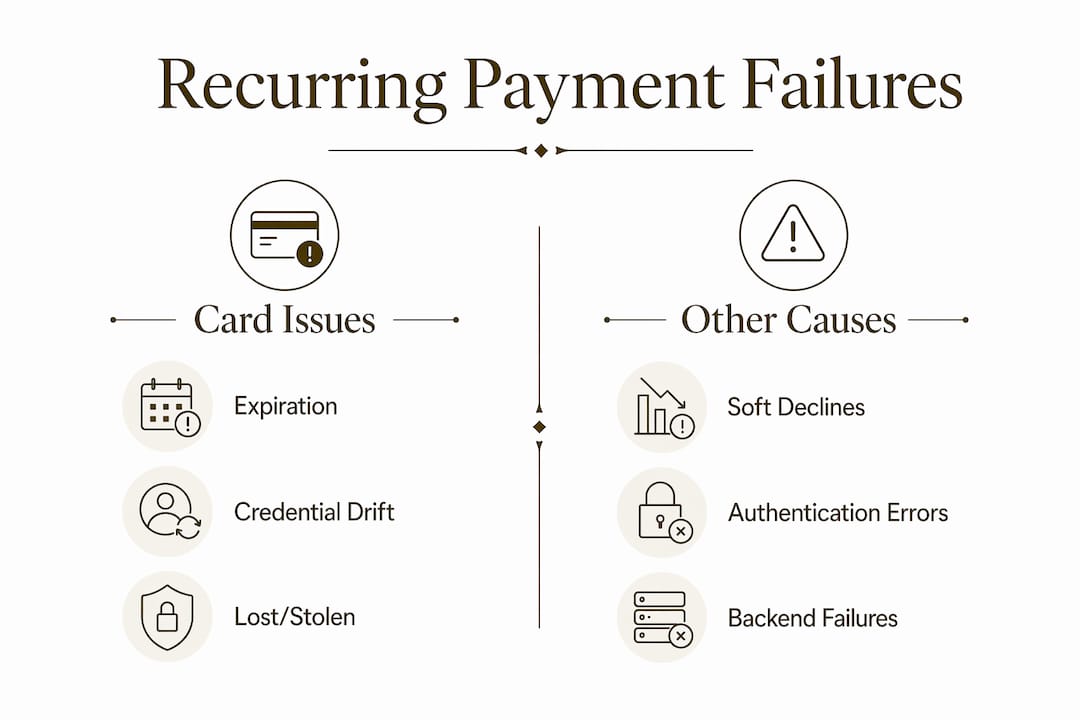

Recurring payment failure is defined as the inability of an automated billing system to successfully charge a customer’s saved payment method on a scheduled date. The four root causes are card status problems, insufficient funds, authentication misconfigurations, and backend system errors. Understanding why recurring payments fail is the first step toward recovering lost revenue and stopping involuntary churn before it compounds. Platforms like Stripe, Visa, and Basis Theory each publish guidance on these failure types, and the data is clear: most failures are preventable with the right retry logic, credential management, and system design.

Why do recurring payments fail? the core causes

Card-related problems are the single most common source of failed subscription payments. Cards expire, get reissued after fraud, or are reported lost or stolen. When your billing system attempts a charge against an outdated card number or expiration date, the issuer returns a hard decline. Hard declines are terminal. They signal that the card cannot be used and should not be retried without updated credentials.

Soft declines work differently. A soft decline means the transaction failed temporarily, not permanently. Insufficient funds, bank-side risk flags, and temporary holds all produce soft declines. These are retryable, but only under the right conditions and within the right timeframe.

The distinction between hard and soft declines matters more than most finance teams realize. Retrying a hard decline wastes processing attempts and can trigger scheme fees. Retrying a soft decline at the right moment recovers real revenue.

- Hard declines: Card reported lost or stolen, account closed, card number invalid

- Soft declines: Insufficient funds, temporary bank hold, do-not-honor flags

- Authentication failures: Off-session charges missing proper setup flags

- Backend errors: Webhook failures, duplicate charges, state management gaps

Pro Tip: Build your decline code library before you build your retry logic. Knowing which codes are terminal versus transient is what separates a recovery engine from a retry loop that burns attempts.

How card expiration and credential drift cause billing failures

Expired and reissued cards create what the industry calls credential drift. This is the gradual divergence between the card credentials your system stores and the credentials the issuer currently recognizes as valid. A customer who signed up 18 months ago may have received two new cards since then without ever updating their billing information.

Account updater tools proactively refresh card credentials before a charge attempt fails. Visa and Mastercard both operate account updater services that push new card numbers and expiration dates to participating merchants. Integrating with these services through a provider like Basis Theory reduces involuntary churn at the source rather than trying to recover it after the fact.

The operational fix is structural, not reactive. Waiting for a card to fail and then emailing the customer to update their payment method is the slowest and least effective recovery path. Automated credential refresh handles the majority of expiration-related failures silently, with no customer friction at all.

When a card is reported lost or stolen, the issuer issues a hard decline. No retry will succeed. Your system needs to detect this code, suppress further retry attempts, and trigger a customer notification requesting a new payment method. Treating a stolen card the same as an insufficient funds error is a common and costly mistake.

Pro Tip: Set up account updater integrations through your payment gateway or vault provider before your subscriber base grows. Retrofitting credential refresh into a large billing system is significantly more complex than building it in from the start.

How insufficient funds and soft declines affect retry success

Insufficient funds is classified as decline code 51 and is one of the most recoverable failure types in recurring billing. The card is valid. The customer relationship is intact. The only problem is timing. Many customers live paycheck to paycheck, and a subscription renewal that hits on the wrong day of the month will fail even for otherwise reliable payers.

Retry and dunning programs recover roughly 50–70% of recoverable failed subscription payments when timing and messaging are handled correctly. That recovery rate represents a significant share of revenue that would otherwise be lost to involuntary churn. A combined window of approximately 14 days with layered communications and retries is the most effective approach.

Here is a practical retry sequence for soft declines caused by insufficient funds:

- Attempt 1: Retry 24 hours after the initial failure. Many customers receive direct deposits within this window.

- Attempt 2: Retry 3 days after the first retry. Send an in-app or email notification alerting the customer to the failed charge.

- Attempt 3: Retry 7 days after the initial failure. Escalate the customer notification to include a direct link to update payment details.

- Attempt 4: Final retry at day 14. If this fails, pause the subscription and send a final recovery email with a clear reactivation path.

Customer communication is not optional in this sequence. Silent retries alone recover a portion of failures, but layered dunning communications, which combine retry attempts with direct customer outreach, consistently outperform retry-only approaches. Customers who know a charge failed are more likely to act than customers who discover their subscription was canceled without warning.

Why authentication errors cause off-session payment failures

Off-session payments are charges that occur without the customer present at checkout. Every recurring billing transaction after the first one is off-session. This distinction matters because issuers apply different authentication standards to off-session charges, and a misconfigured payment setup will fail these checks even when the card is valid and the funds are available.

Stripe addresses this directly. Using during the initial payment intent signals to the issuer that the card will be charged in the future without the customer present. Without this flag, the issuer may reject subsequent charges as unauthorized, even though the customer originally consented to recurring billing.

The fix requires proper setup at the point of initial enrollment, not at the point of failure:

- Store payment method IDs securely after the initial authorized transaction

- Set the correct off-session flag during the initial charge or setup intent

- Detect authentication-required errors on subsequent charges and send the customer a re-authentication link

- Never retry an authentication-required decline without first resolving the underlying credential or consent issue

Authentication failures look like recurring payment errors on the surface, but they are often authentication mismatches caused by missing setup configuration. Proper off-session billing setup prevents most of these failures before they reach the retry stage.

Pro Tip: If you see a spike in authentication-required declines after migrating to a new payment gateway, check whether your initial payment intents are being created with the correct future-use flags. This is one of the most common post-migration failure patterns.

What backend system failures do to recurring billing reliability

Backend complexity is an underestimated contributor to recurring billing failures. Scheduling errors, webhook processing gaps, and state management problems all create failures that look like payment errors but originate inside your own infrastructure.

Backend recurring billing failures stem from complex event workflows where timing errors create duplicate charges and revenue loss. A retry that fires twice because a webhook was processed twice produces a duplicate charge. A retry that never fires because a webhook was dropped produces a missed recovery attempt. Both outcomes damage revenue and customer trust.

| Backend Failure Type | Root Cause | Business Impact |

|---|---|---|

| Duplicate charges | Non-idempotent retry logic | Customer disputes, chargebacks |

| Missed retries | Dropped or unprocessed webhooks | Unrecovered failed payments |

| State inconsistency | Race conditions in event processing | Incorrect subscription status |

| Scheduling drift | Clock skew or job queue failures | Charges firing on wrong dates |

Reliable payment architectures treat payments as event-driven state machines with idempotency and webhook deduplication built in. Idempotency means that processing the same webhook event twice produces the same result as processing it once. Without idempotency, any retry or redelivery in your event pipeline becomes a risk for duplicate charges.

A payment failure today can become a customer support problem next week if backend reliability is poor. The customer sees a failed charge, then a duplicate charge, then a canceled subscription they did not expect. Each of those touchpoints generates a support ticket, a potential chargeback, and a higher probability of permanent cancellation.

Observability is the operational fix. Instrument your payment engine to log every state transition, every webhook receipt, and every retry attempt. When something goes wrong, you need to know exactly what happened and when.

How network rules and decline codes shape your retry policy

Payment networks publish specific rules about how many times you can retry a declined transaction. Ignoring these rules does not just waste retry attempts. It generates fees and can result in scheme penalties that compound over time.

Visa prohibits retrying declined transactions 15 or more times within a 30-day period. Fines apply from the 16th attempt onward. This rule exists to prevent merchants from hammering issuers with retry loops that the issuer has already signaled will not succeed.

Decline codes are signals, not just error messages. Each code tells you something specific about why the transaction failed and what action, if any, is appropriate. Treating all declines as equivalent and retrying on a fixed schedule is the fastest way to exhaust your permitted attempts and incur penalties.

| Decline Code | Type | Retry Appropriate? |

|---|---|---|

| 51 (Insufficient Funds) | Soft | Yes, after timing delay |

| 54 (Expired Card) | Hard | No, update credentials first |

| 41 (Lost Card) | Hard | No, request new payment method |

| 05 (Do Not Honor) | Soft | Yes, with limit |

| 14 (Invalid Card Number) | Hard | No, update credentials first |

Integrating decline code logic into your retry engine means your system makes a decision on every failure, not just a default retry. Terminal codes suppress retries and trigger customer outreach. Transient codes schedule retries within network-permitted windows. This approach reduces fees, improves recovery rates, and keeps your merchant account in good standing.

Key takeaways

Recurring payment failures are recoverable in most cases when your system correctly identifies the failure type and responds with the right action.

| Point | Details |

|---|---|

| Hard vs. soft declines | Hard declines require credential updates; soft declines are retryable with proper timing. |

| Credential drift prevention | Account updater tools reduce card expiration failures before they reach the retry stage. |

| Retry recovery rates | Layered dunning programs recover 50–70% of failed payments within a 14-day window. |

| Off-session setup | Setting at enrollment prevents most authentication failures. |

| Network retry limits | Visa caps retries at 15 per 30 days; exceeding this triggers fines from the 16th attempt. |

What i’ve learned about retry strategy after years in payment operations

Most ecommerce teams treat retry logic as an afterthought. They set a fixed schedule, maybe three attempts over a week, and call it done. That approach leaves a significant share of recoverable revenue on the table.

The teams that consistently outperform on payment recovery treat decline codes as a decision tree, not a uniform trigger. They retry code 51 on a timing-sensitive schedule tied to typical payroll cycles. They suppress retries entirely on code 41. They send re-authentication links the moment they see an authentication-required error. Every code gets a specific response.

The second thing I’ve seen make a real difference is combining silent retries with proactive customer communication. Customers who receive a clear, non-alarming notification that their payment failed and who are given a direct link to resolve it convert at a much higher rate than customers who only find out when their access is cut off. The tone of that communication matters too. Accusatory or urgent messaging drives cancellations. Helpful, low-friction messaging drives payment updates.

For subscription merchants in high-risk categories, including supplement brands and nutraceutical businesses, the stakes are higher because acquiring relationships are harder to replace. A spike in chargebacks from retry abuse or a pattern of excessive declines can put your merchant account at risk. Building a compliant, intelligent retry engine is not just a revenue optimization. It is a risk management requirement.

Measure everything. Track your recovery rate by decline code, by retry attempt number, and by customer segment. The data will tell you exactly where your retry logic is working and where it is not.

— Peter

How Davincipay helps you reduce failed recurring payments

Recurring billing failures cost subscription merchants real revenue every month. Davincipay specializes in payment processing for high-risk and complex ecommerce businesses, including subscription merchants who need reliable retry infrastructure, fraud prevention, and acquiring relationships that hold up under volume.

Davincipay’s payment solutions are built for merchants who cannot afford to lose transactions to preventable failures. From chargeback mitigation to gateway configuration support, the platform addresses the full stack of recurring payment challenges. If you run a subscription business and want a payment infrastructure that is built to recover failed charges and protect your merchant account, apply now and get started with a team that understands your business. You can also explore the full range of payment processing solutions Davincipay offers for high-risk ecommerce.

FAQ

What is the most common reason recurring payments fail?

Expired or reissued cards are the leading cause of recurring payment failures. Account updater tools from providers like Basis Theory can refresh credentials automatically before a charge attempt fails.

How many times can you retry a declined recurring payment?

Visa limits retries to 15 attempts within a 30-day period. Retrying beyond this threshold triggers fines starting from the 16th attempt, so your retry logic must track attempt counts per transaction.

What is the difference between a hard and soft decline?

A hard decline is terminal and means the card cannot be charged without updated credentials or a new payment method. A soft decline is temporary and the transaction may succeed on a later retry attempt.

How do retry programs recover failed subscription payments?

Dunning programs that combine timed retries with customer notifications recover roughly 50–70% of recoverable failed payments within a 14-day window. Timing retries around typical payroll deposit dates improves recovery rates for insufficient funds failures.

Why do off-session recurring charges fail even with a valid card?

Off-session charges fail when the initial payment was not configured for future use. Using in Stripe during enrollment signals to the issuer that the card will be charged without the customer present, preventing authentication rejections on subsequent billing cycles.

.webp)