.png)

High-risk merchants are defined as businesses that payment platforms flag for elevated fraud exposure, chargeback frequency, or regulatory complexity, making them costly and operationally demanding to support. The core reason why high-risk merchants challenge platforms comes down to three converging pressures: tightening card network enforcement programs, reputational constraints from acquiring banks, and compliance demands that require continuous operational controls. In 2026, updates to Visa’s VAMP program and Mastercard’s ECP program have raised the stakes further. Understanding these pressures is the first step toward managing them.

Why high-risk merchants challenge platforms: the core mechanics

The challenges faced by high-risk merchants on payment platforms are not arbitrary. They are driven by measurable risk metrics that card networks and acquiring banks monitor monthly. When your dispute or fraud ratio exceeds defined thresholds, the consequences escalate fast: fines, reserves, volume caps, and in the worst cases, placement on the MATCH list, which effectively blacklists you from standard processing.

Visa tightened its VAMP “Excessive Merchant” threshold from 2.2% to 1.5% effective April 1, 2026. That reduction cuts the margin for error nearly in half, meaning merchants who were previously compliant may now exceed limits without changing anything about their business model. The threshold applies once a merchant reaches 1,500 combined fraud and dispute events per month, so volume compounds the risk.

Mastercard’s ECP program triggers enforcement at 100+ chargebacks with a 1.5% to 2.99% monthly chargeback-to-transaction ratio. Fines escalate from the second month onward, and exiting the program requires staying below thresholds for three consecutive months. That exit requirement alone can trap merchants in a fine cycle for a quarter or more.

A merchant with a 1.6% fraud and dispute ratio and 2,000 monthly events faces $16,000 in monthly VAMP fines before any other fees. That figure illustrates why platforms treat high-risk accounts as liabilities rather than revenue opportunities.

Pro Tip: Track your fraud and dispute ratios weekly, not monthly. By the time a monthly statement surfaces a problem, you may already be inside a monitoring program with no fast exit.

How acquiring bank constraints limit support for high-risk merchants

Payment platforms do not operate independently. They process transactions through acquiring banks, and those banks set internal risk appetites that directly control which merchants a platform can support. When an acquiring bank restricts a category, the platform has no choice but to decline or terminate merchants in that space, regardless of the individual merchant’s actual performance.

Merchant rejection often traces back to reputational risk and partner bank license constraints rather than the merchant’s own fraud data. A nutraceutical brand with a clean dispute record can still be declined because its acquiring bank has a blanket policy against supplement merchants. This is one of the most frustrating high-risk business platform difficulties merchants encounter.

The problem runs deeper than individual bank policies. Legacy risk frameworks categorize entire verticals as high-risk despite improved compliance and fraud controls by individual merchants. Subscription services, telehealth providers, and supplement brands are grouped by category stereotype rather than actual performance data. That institutional inertia means a well-run business pays the same access penalty as a poorly managed one.

Here is what this looks like in practice for merchants facing these issues:

The distinction between a high-risk platform and a standard platform is not just pricing. It is the depth of acquiring relationships and the willingness to advocate for your account when a bank’s automated systems flag a concern.

How PCI DSS 4.0.1 adds compliance pressure to high-risk merchant platforms

Compliance is no longer a once-a-year audit event. PCI DSS 4.0.1 mandates continuous operation and ongoing evidence of security controls, with the full standard enforced since March 31, 2025. For high-risk merchants and the platforms that support them, this shift from point-in-time audits to continuous risk management adds significant operational overhead.

The standard now requires active monitoring of payment page scripts, log reviews, and documented evidence that controls are operating at all times, not just during an annual assessment window. E-commerce merchants are specifically affected by requirements around third-party scripts on checkout pages, which are a common vector for card-skimming attacks. If your payment page loads any external JavaScript, you need a formal inventory and change-detection process in place.

Platforms supporting high-risk merchants carry a compounded compliance burden. They must maintain their own PCI DSS certification while also verifying that merchants in their portfolio meet requirements. A single non-compliant merchant can create liability exposure for the entire platform. This is why many standard processors simply decline high-risk categories rather than absorb the compliance management cost.

Pro Tip: Request a copy of your payment platform’s current PCI DSS Attestation of Compliance (AOC). If they cannot produce one on request, treat that as a serious red flag about their operational standards.

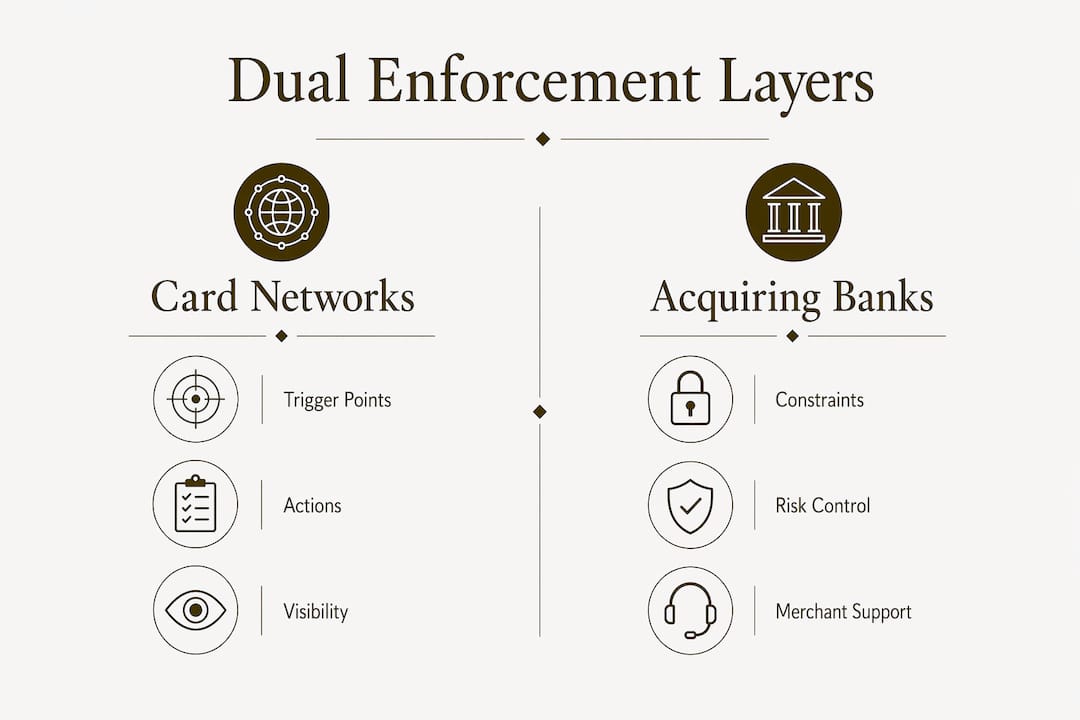

What is the dual-layer enforcement system merchants face?

Payment enforcement operates on two distinct levels, and most merchants only understand one of them. Card network programs like Visa VAMP and Mastercard ECP set the formal thresholds that define when a merchant enters a monitoring program. But providers enforce stricter portfolio controls through automated systems that can act well before a merchant reaches a network-level threshold.

The table below shows how these two enforcement layers differ in practice:

Enforcement layerTrigger pointTypical actionMerchant visibilityCard network (Visa VAMP)1.5% fraud+dispute ratio, 1,500+ eventsFormal monitoring, fines, MATCH riskMonthly reporting, formal noticeCard network (Mastercard ECP)100+ chargebacks, 1.5%+ ratioEscalating fines, program enrollmentMonthly reporting, formal noticeProvider automationOften 0.5% to 0.9% ratio internallyReserve increase, freeze, volume capOften no advance noticeAcquirer portfolio level0.5% above standard, 0.7% excessiveMerchant-level intervention, terminationVaries by acquirer

Acquirers must remediate portfolios above 0.5% “above standard” and 0.7% “excessive” thresholds, and they frequently enforce stricter merchant-level limits to protect their own standing with card networks. This means you can be fully compliant with Visa’s published rules and still face a freeze because your processor’s internal model flagged your account.

This dual-layer system is why issues for high-risk payment processors are more complex than merchants often realize. Knowing the network rules is necessary but not sufficient. You also need to understand your specific processor’s internal risk tolerance and how their automated systems are configured.

How to reduce the challenges high-risk merchants face on platforms

Managing your risk profile is an active discipline, not a passive one. The merchants who maintain stable processing accounts treat dispute prevention and compliance as core business operations, not afterthoughts.

Pro Tip: Ask any prospective payment processor specifically which acquiring banks they use for your merchant category. Vague answers about “multiple banking partners” often mean limited options and higher termination risk.

Peter’s take: why the system is harder than it needs to be

The honest truth about why high-risk merchants struggle with payment platforms is that the system was not designed with them in mind. Card network enforcement programs, acquiring bank risk frameworks, and compliance standards were built around the median merchant. High-risk verticals were added as exceptions, and the infrastructure reflects that.

What frustrates me most is the legacy categorization problem. I have seen supplement brands with dispute rates below 0.3% get declined by processors who apply blanket category restrictions. The high-risk label often reflects institutional inertia rather than actual merchant performance. That is a real cost to real businesses, and it is not going away on its own.

The 2026 Visa VAMP tightening is a signal worth taking seriously. Measurable monthly fraud and dispute metrics are now the primary enforcement lever, which means small operational lapses can become expensive fast. The merchants who will navigate this environment well are the ones who treat risk management as a revenue protection strategy, not a compliance checkbox.

My advice: stop waiting for platforms to accommodate you and start selecting platforms built for your category. The difference between a processor who tolerates high-risk merchants and one who specializes in them is not marginal. It is the difference between account stability and a termination notice at the worst possible moment.

How Davincipay helps high-risk merchants process with confidence

Davincipay is built specifically for the merchants this article describes. If you operate in nutraceuticals, supplements, telehealth, subscriptions, or another regulated vertical, Davincipay provides the acquiring relationships, chargeback mitigation tools, and compliance support your business actually needs. The platform includes fraud prevention infrastructure, pre-dispute resolution integrations, and underwriting support designed for high-risk account stability. Davincipay’s team understands the dual-layer enforcement environment and works proactively to keep your account in good standing. Explore payment solutions for high-risk businesses or apply now to get started with a processor built for your category.

FAQ

What makes a merchant “high-risk” to payment platforms?

Payment platforms classify merchants as high-risk based on elevated chargeback rates, fraud exposure, regulatory complexity, or industry category. Verticals like nutraceuticals, telehealth, and subscription services are frequently flagged regardless of individual merchant performance.

What is the Visa VAMP threshold in 2026?

Visa tightened the VAMP Excessive Merchant threshold to 1.5% effective April 1, 2026, down from 2.2%. Merchants with 1,500 or more combined fraud and dispute events per month are subject to formal monitoring and escalating fines.

Can a merchant be terminated even if they follow card network rules?

Yes. Providers enforce internal risk controls that are often stricter than card network thresholds. A merchant compliant with Visa or Mastercard rules can still face a freeze or termination due to a processor’s automated portfolio management systems.

How does PCI DSS 4.0.1 affect high-risk merchants specifically?

PCI DSS 4.0.1 requires continuous evidence of security controls rather than annual audits. High-risk merchants must actively monitor payment page scripts, maintain log reviews, and document ongoing compliance, adding operational overhead that standard merchants rarely face at the same intensity.

What is the fastest way to reduce chargeback exposure?

Deploy device fingerprinting, use pre-dispute resolution tools like Ethoca or Verifi, and clarify billing descriptors and refund policies at checkout. These three steps address the majority of dispute sources before they reach formal chargeback status.

Key takeaways

High-risk merchants face platform challenges because card network enforcement, acquirer risk constraints, and continuous compliance requirements create compounding operational pressure that standard processors are not equipped to manage.

PointDetailsVAMP threshold tightened in 2026Visa reduced the Excessive Merchant limit to 1.5%, cutting the margin for error nearly in half for high-volume merchants.Acquirer constraints drive rejectionsReputational risk and bank license limits cause merchant declines that have nothing to do with individual fraud performance.Dual-layer enforcement creates hidden riskProviders act on internal thresholds stricter than network rules, meaning compliance with Visa or Mastercard does not guarantee account stability.PCI DSS 4.0.1 requires continuous controlsCompliance is now an ongoing operational function, not an annual audit, adding sustained overhead for high-risk merchant platforms.Specialized processors reduce exposureWorking with a processor built for high-risk verticals provides acquiring depth, chargeback tools, and compliance support that standard platforms cannot offer.

.webp)