.png)

A payment gateway is defined as a regulated technology intermediary that encrypts, tokenizes, and routes customer payment data between a merchant, acquiring bank, and issuing bank to authorize transactions in real time. The role of payment gateway in ecommerce extends far beyond a checkout form. Providers like Stripe and Braintree handle authorization, fraud screening, and settlement within seconds, making them the operational backbone of every online sale. Your gateway choice directly affects approval rates, PCI compliance exposure, and whether customers complete their purchase or abandon their cart.

How payment gateways work in the online transaction process

A payment gateway handles multiple critical functions in under 2 seconds, making it far more than a passive data pipe. Understanding the transaction flow helps you diagnose approval failures, reduce friction, and build a more reliable checkout.

Here is the sequence every online payment follows:

Gateways communicate authorization or decline in real time, usually within a few seconds in standard ecommerce flows. That speed is not accidental. It depends on reliable API connections, proper retry logic, and idempotency keys that prevent duplicate charges when a network timeout triggers a retry.

Pro Tip: Always implement idempotency keys in your gateway API calls. Without them, a customer’s browser refresh or a network timeout can trigger a duplicate charge, which generates chargebacks and damages trust.

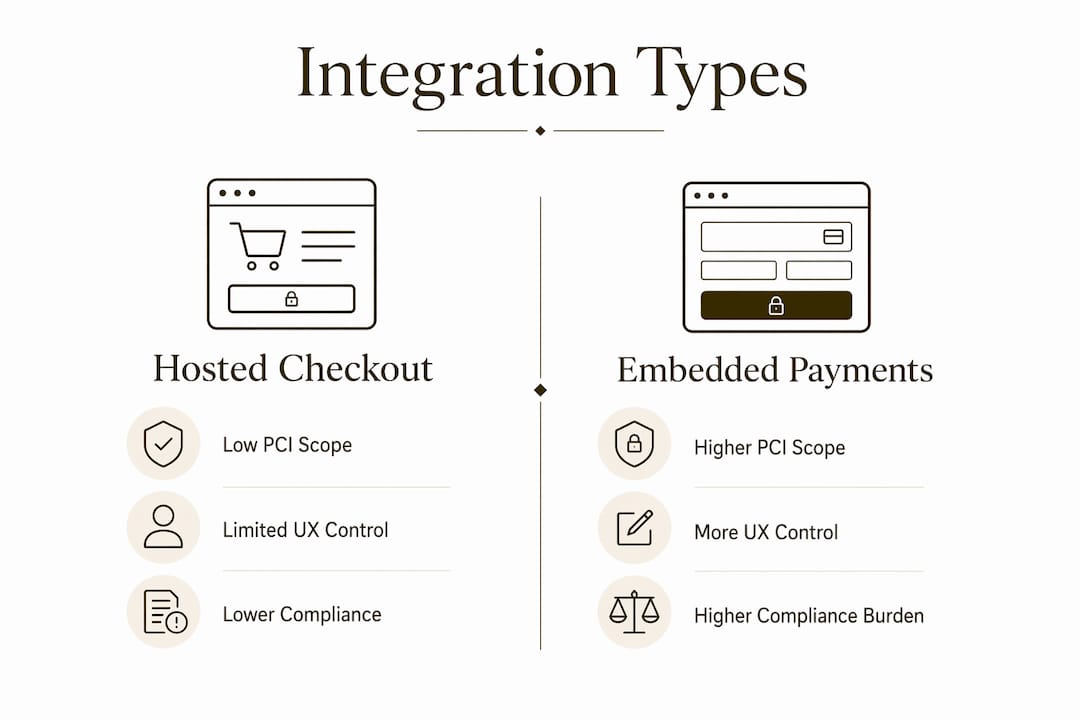

What integration type means for PCI compliance and user experience

Your architecture choice for payment integration determines your PCI scope and compliance responsibilities under a shared responsibility model. This is one of the most consequential decisions you will make when building your checkout.

Integration typePCI DSS scopeUX controlCompliance burdenHosted checkout (e.g., Stripe Checkout, Shopify Payments)SAQ A (lowest)LimitedLowEmbedded/inline form with gateway JavaScriptSAQ A-EP or SAQ DHighModerate to highFull API integration (custom card form)SAQ D (highest)FullVery high

Hosted checkout qualifies merchants for SAQ A because the payment page is served entirely by the gateway provider. Your servers never touch raw card data. Stripe Checkout and Shopify’s native checkout both operate this way. The trade-off is that you have less control over the visual design and flow of the payment step.

Embedded payments, where you render a card input field using the gateway’s JavaScript library, give you more design control. However, embedded payment forms increase PCI DSS scope because your systems become involved in cardholder data handling, even indirectly through the scripts you load. This pushes you into SAQ A-EP or SAQ D territory, requiring quarterly vulnerability scans and more rigorous annual assessments.

For most ecommerce merchants under $50 million in annual revenue, hosted checkout is the right default. You reduce compliance cost, offload security responsibility to your gateway provider, and still deliver a fast checkout experience. Embedded forms make sense when your brand requires tight UX consistency and you have the engineering resources to maintain compliance.

Pro Tip: If you use embedded JavaScript payment fields, monitor all third-party scripts loaded on your checkout page continuously. A compromised script from any vendor on that page can expose card data, a risk that falls squarely on you under PCI DSS.

How payment gateways affect conversion rates and checkout friction

Online cart abandonment hit 72% in early 2026, with 22% of abandoners citing a lengthy or complicated checkout as the primary reason. That statistic means your gateway configuration is a direct revenue lever, not just an IT concern.

Payment gateways influence conversion in several specific ways:

You can also reduce abandonment by optimizing your checkout flow to minimize steps and surface the most relevant payment methods first. Gateway configuration, not just gateway selection, determines how much of this optimization is possible.

Choosing and optimizing a payment gateway for your business

Selecting a payment gateway is not a one-time decision. It requires ongoing evaluation as your transaction volume, product mix, and customer geography evolve. Here is what to prioritize:

The authorization routing strategy your gateway uses also matters. Merchants with high-risk products or international customer bases need gateways with multiple acquiring relationships so that a single bank’s risk appetite does not cap your approval rate.

Pro Tip: Test your gateway’s non-happy paths before launch: simulate declines, expired cards, insufficient funds, and webhook delivery failures. Most integration failures surface in these edge cases, not in successful payment flows.

Key takeaways

A payment gateway is the single most operationally critical component in your ecommerce stack, directly controlling authorization speed, fraud exposure, PCI compliance scope, and checkout conversion.

PointDetailsGateway functionGateways encrypt, tokenize, and route payment data between merchant and banks in real time.Integration type determines complianceHosted checkout reduces PCI scope to SAQ A; embedded forms increase your compliance burden significantly.Cart abandonment is a gateway problem72% cart abandonment in 2026 means checkout friction is a direct revenue issue you can address through gateway configuration.Local payment methods drive conversionSupporting iDEAL, Pix, SEPA, and similar local rails is critical for cross-border ecommerce revenue.Custom builds are rarely justifiedBuild your own gateway only above $50M to $100M GMV; integrate proven providers below that threshold.

What most merchants get wrong about payment gateways

Most ecommerce entrepreneurs I work with treat their payment gateway as a commodity. They pick the first option their platform recommends, configure the minimum required settings, and move on. That approach costs real money.

The biggest misconception is that a gateway is just a checkout button. It is not. It is a regulated intermediary that influences whether your transactions get approved, how much fraud you absorb, and what your compliance obligations look like. Merchants who understand this treat their gateway configuration as a growth lever, not a setup task.

The second mistake I see constantly is ignoring the PCI implications of integration choices. Merchants add an embedded card form because it looks cleaner, without realizing they have just expanded their compliance scope and taken on liability they are not prepared to manage. Your architecture choice is a compliance decision first and a design decision second.

In 2026, the merchants winning at checkout are the ones monitoring authorization rates by card type, by geography, and by device. They are testing fallback acquirers. They are validating that their 3DS2 configuration challenges the right transactions without blocking good customers. These are not advanced tactics. They are table stakes for any merchant serious about growth.

How Davincipay helps ecommerce merchants process payments reliably

Davincipay specializes in payment processing for ecommerce merchants who need more than a standard gateway setup. Whether you operate in nutraceuticals, supplements, telehealth, or subscription commerce, Davincipay provides access to domestic and international acquiring relationships, fraud prevention tools, and chargeback mitigation support built for complex merchant categories.

Davincipay’s infrastructure supports high-risk payment processing with PCI compliance guidance, multi-currency support, and authorization routing strategies designed to maximize approval rates. If your current gateway is limiting your approvals or leaving you exposed on compliance, Davincipay can help you build a more reliable payment stack. Apply now to get started with a payment solution built for your business.

FAQ

What is the role of a payment gateway in ecommerce?

A payment gateway encrypts and transmits customer payment data between the merchant, acquiring bank, and issuing bank to authorize transactions in real time. It also handles fraud screening, tokenization, and settlement coordination, making it the core transaction infrastructure for any online store.

How does a payment gateway differ from a payment processor?

A payment gateway is the technology layer that securely transmits payment data, while a payment processor is the financial institution that executes the actual movement of funds between banks. Many providers bundle both functions, but they are distinct roles in the transaction chain.

What is the fastest way to reduce PCI compliance burden?

Use a hosted checkout solution like Stripe Checkout or Shopify Payments, which qualifies your business for SAQ A, the lowest PCI DSS compliance tier. This offloads card data handling entirely to the gateway provider and removes your servers from the compliance scope.

Why do payment gateways affect cart abandonment rates?

Slow authorization, excessive checkout steps, and missing local payment methods all increase abandonment. With cart abandonment at 72% in early 2026, gateway configuration directly determines how many customers complete their purchase.

When should an ecommerce merchant build a custom payment gateway?

Custom gateway development is only economically justified for merchants processing above $50 million to $100 million in annual GMV. Below that volume, integrating with an established provider delivers better cost efficiency and faster time to market.

.webp)