.png)

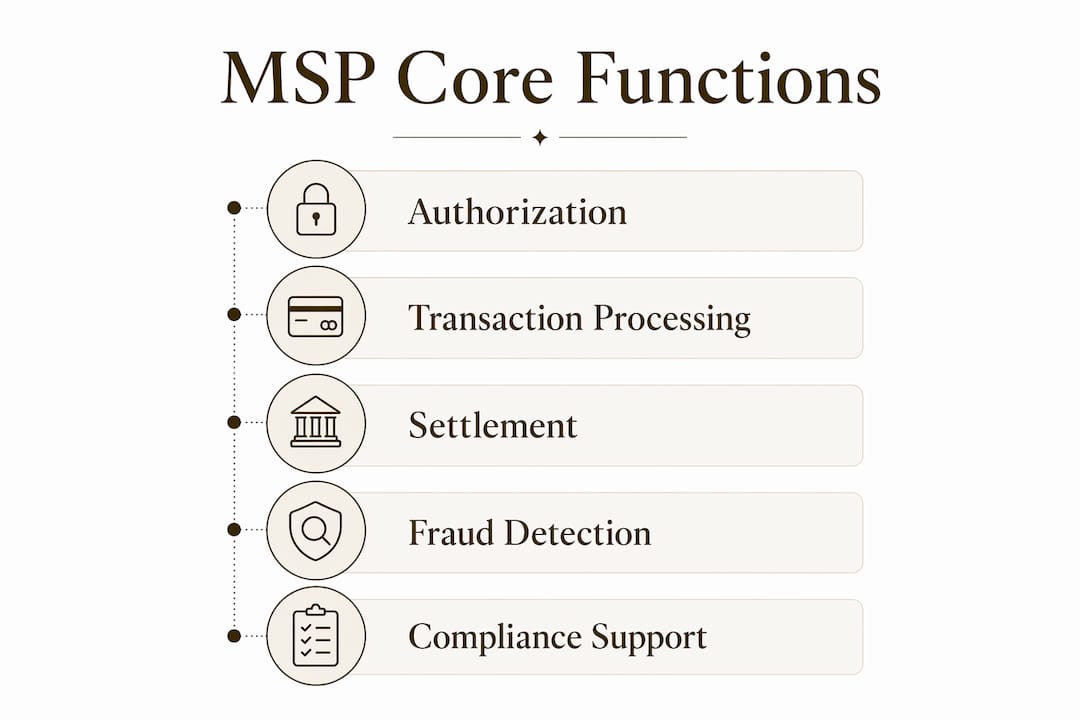

A merchant services provider (MSP) is the intermediary that enables businesses to accept, process, and settle electronic card payments by connecting merchants with acquiring banks and card networks like Visa and Mastercard. Without an MSP, your ecommerce store or subscription business cannot accept credit cards, debit cards, or digital wallets. The role of merchant services provider goes far beyond a simple payment button. MSPs manage the entire transaction lifecycle, from authorization to settlement, while also handling fraud detection, chargeback disputes, PCI compliance, and operational reporting. For high-risk ecommerce brands, nutraceutical companies, and subscription merchants, choosing the right MSP is one of the most consequential infrastructure decisions you will make.

How do merchant services providers work to process and settle payments?

MSPs capture transaction data and route it through card networks to issuing banks for authorization, then handle settlement typically within 24–48 hours. That timeline directly affects your cash flow. A two-day funding cycle is standard, but reserve policies and risk flags from acquiring banks can extend holds significantly for high-risk merchants.

The payment flow works in a clear sequence:

- Customer initiates payment. The customer enters card details at checkout or on a subscription billing page.

- Gateway captures and encrypts data. The payment gateway tokenizes the card data and sends it to the MSP.

- MSP routes the authorization request. The MSP forwards the request through the card network (Visa, Mastercard) to the customer’s issuing bank.

- Issuing bank approves or declines. The bank checks available funds and fraud signals, then returns an authorization code.

- MSP confirms the transaction. The approval flows back through the network to your checkout in seconds.

- Settlement occurs within 24–48 hours. The MSP batches approved transactions and initiates fund transfers to your merchant account.

- Funds move to your business bank account. The merchant account holds funds temporarily during processing before releasing them to your checking account.

The distinction between a merchant account and a business bank account matters. A merchant account is not where you operate your business finances. It is a holding account that exists solely to facilitate secure payment processing. Your MSP manages this account and controls the release of funds based on risk assessments and settlement schedules.

Pro Tip: Ask any MSP candidate to show you their exact settlement schedule and reserve policy in writing before signing. Vague answers on funding timelines are a red flag for high-risk merchants.

Understanding that settlement timing and risk decisions rest with acquiring banks, not just your MSP, helps you interpret funding holds and dispute outcomes more accurately.

What key services do merchant services providers offer beyond basic payments?

The functions of merchant services extend well past moving money from point A to point B. A capable MSP delivers a suite of tools that protect your revenue and reduce operational complexity.

- Fraud detection and prevention. AI and machine learning now power fraud monitoring across most major MSPs. These systems flag suspicious transaction patterns in real time, reducing revenue losses without adding friction to legitimate customers. For subscription businesses with recurring billing, this protection is non-negotiable.

- Chargeback and dispute management. MSPs provide tools and dedicated support to help you respond to chargebacks with evidence. High chargeback ratios can get your merchant account terminated, so active dispute management is a core merchant service provider benefit.

- PCI DSS compliance support. PCI compliance is a shared responsibility between merchants and MSPs. Your MSP can reduce your compliance scope, but it does not eliminate your obligations. The exact division depends on how cardholder data flows through your systems and which components your MSP controls.

- Unified reporting dashboards. Strong MSPs consolidate sales data, transaction history, refund tracking, and customer engagement metrics into a single platform. That visibility lets you make faster, more accurate business decisions.

- Payment gateway and POS integration. MSPs integrate gateways for online transactions and point-of-sale terminals for in-person sales, giving omnichannel merchants a single payment infrastructure.

| Service | What it does for your business |

|---|---|

| Fraud detection | Blocks suspicious transactions before they cost you revenue |

| Chargeback management | Reduces dispute losses and protects your merchant account standing |

| PCI compliance support | Lowers your compliance burden through shared responsibility frameworks |

| Unified reporting | Combines sales, refunds, and customer data in one dashboard |

| Gateway integration | Connects your checkout, subscriptions, and POS to one payment system |

Pro Tip: Before signing with any MSP, request a sample compliance responsibility matrix. Knowing exactly which PCI obligations remain yours prevents costly surprises during audits.

How to choose the right merchant services provider for your business?

Choosing a merchant services provider is a decision that affects your revenue, your customer experience, and your operational workload every single day. The wrong choice costs you money through fees, fraud losses, and poor support. The right choice functions as a growth platform.

Focus on these criteria when evaluating providers:

- Fee transparency. Interchange-plus pricing is more transparent than flat-rate or tiered models. Understand every fee: transaction fees, monthly fees, chargeback fees, and early termination penalties. Hidden fees erode margins fast.

- Fraud protection effectiveness. Ask for specifics on how the MSP detects fraud. Generic answers about “advanced tools” are not enough. You need to know whether they use machine learning, velocity checks, and 3D Secure authentication.

- Chargeback management tools. For subscription and ecommerce merchants, chargeback ratios above 1% trigger card network warnings. Your MSP should offer proactive alerts, dispute response templates, and dedicated support staff.

- Scalability. Your MSP must handle volume spikes, new product lines, and international expansion without requiring a platform change. Choosing MSPs involves software decisions that integrate payments with inventory, sales, and customer data for long-term operational efficiency.

- Customer support quality. Payment failures happen at the worst times. You need 24/7 access to knowledgeable support, not a chatbot. Ask about dedicated account managers for high-risk merchants.

- Integration capabilities. Your MSP must connect cleanly with your ecommerce platform (Shopify, WooCommerce, Magento), subscription billing software, and CRM. Poor integration creates data gaps and manual reconciliation work.

The importance of merchant services selection compounds over time. A provider that works at $50,000 per month in volume may create serious bottlenecks at $500,000 per month. Evaluate scalability before you need it.

How does partnering with an MSP impact your profitability and efficiency?

The right MSP directly improves your bottom line. The wrong one quietly drains it through fees, fraud losses, and operational friction.

- Cash flow. Settlement speed matters. A 24–48 hour funding cycle keeps working capital available. Rolling reserves, which some MSPs require for high-risk merchants, can tie up 5–10% of monthly volume for months. Negotiate reserve terms before you sign.

- Fraud cost reduction. Fraud losses do not just hit your revenue directly. They trigger chargebacks, which carry fees and damage your merchant account standing. AI-driven fraud tools from a strong MSP reduce both the direct loss and the downstream chargeback exposure.

- Operational efficiency. A solid MSP acts as a platform supporting sales visibility, inventory management, and customer engagement. When your payment data, refund history, and customer records live in one system, your team spends less time reconciling spreadsheets and more time growing the business.

- Decision-making speed. Unified reporting gives you real-time visibility into which products, channels, and customer segments drive the most revenue. That data lets you act on trends within hours, not weeks.

“Merchant services should be viewed as infrastructure that unifies payments with operations, providing a business platform rather than just a checkout system.” — Bank of America Business Resources

The integration design of your payment system also determines your PCI compliance scope. Merchants who rely on MSP-hosted payment pages and tokenization carry far less compliance burden than those who handle raw card data directly. That reduction in scope translates to lower audit costs and reduced liability.

Key Takeaways

A merchant services provider is the operational backbone of any ecommerce or subscription business that accepts electronic payments, and choosing the right one determines your cash flow, fraud exposure, and long-term growth capacity.

| Point | Details |

|---|---|

| MSPs manage the full payment lifecycle | From authorization through settlement, MSPs handle every step between your customer and your bank account. |

| Settlement typically takes 24–48 hours | Funding timelines and reserve policies directly affect your working capital and cash flow planning. |

| Fraud and chargeback tools are core MSP functions | AI-driven fraud detection and dispute management protect revenue and preserve your merchant account standing. |

| PCI compliance is shared, not outsourced | Your MSP reduces your compliance scope but does not eliminate your obligations. Verify responsibility matrices before signing. |

| Provider selection is a long-term infrastructure decision | Evaluate fees, scalability, integration, and support quality before committing. The wrong MSP costs you more than money. |

Why I think most businesses underestimate their MSP choice

After working with ecommerce and subscription merchants across nutraceuticals, telehealth, and high-growth direct-to-consumer brands, I have seen the same mistake repeated: businesses treat their MSP like a utility. They pick whoever approves them fastest and move on.

That approach works until it doesn’t. The merchants who get burned are the ones who discover their MSP has a 180-day rolling reserve policy buried in the contract, or that their “fraud protection” is just a basic velocity filter with no machine learning behind it. By the time those problems surface, the merchant is already locked in.

The businesses that scale well treat their MSP as a core vendor relationship, not a commodity. They negotiate reserve terms upfront. They ask hard questions about chargeback thresholds and what happens when they breach them. They verify, in writing, exactly which PCI obligations their MSP covers and which ones remain theirs.

The other thing I have seen consistently: merchants who invest in MSPs with unified reporting make better decisions faster. When your payment data, subscription metrics, and refund rates live in one dashboard, you stop flying blind. You see which acquisition channels produce customers who churn and charge back, and you cut them before they damage your merchant account.

Your MSP is not just processing payments. It is shaping your cash flow, your compliance posture, and your operational visibility every single day. Treat that relationship accordingly.

— Peter

Davincipay’s payment solutions for high-risk ecommerce merchants

High-risk and subscription merchants face challenges that standard MSPs are not built to handle. Elevated chargeback ratios, complex billing models, and regulatory scrutiny require a provider with real expertise in your industry.

Davincipay specializes in payment processing for high-risk businesses, including ecommerce brands, telehealth companies, nutraceutical merchants, and subscription businesses. Davincipay provides domestic and international acquiring relationships, payment gateway integration, AI-powered fraud prevention, and active chargeback mitigation. You get dedicated underwriting support and account management built for merchants who need more than a generic payment solution. If your business needs a reliable, compliant payment infrastructure, apply now and get your account reviewed by a specialist who understands your industry.

FAQ

What is the role of a merchant services provider?

A merchant services provider enables businesses to accept, process, and settle electronic payments by connecting merchants with acquiring banks and card networks. MSPs also manage fraud detection, chargeback disputes, PCI compliance support, and payment reporting.

How long does it take for an MSP to settle funds?

Settlement typically occurs within 24–48 hours after authorization. High-risk merchants may face longer holds or rolling reserves depending on their MSP’s risk assessment and acquiring bank policies.

What is the difference between a merchant account and a business bank account?

A merchant account is a temporary holding account that processes and clears payment transactions before funds transfer to your business checking account. It is managed by your MSP and is separate from your operating finances.

How does PCI compliance work with a merchant services provider?

PCI compliance is a shared responsibility between the merchant and the MSP. Your provider can reduce your compliance scope through tokenization and hosted payment pages, but your obligations do not disappear entirely. The exact split depends on how cardholder data flows through your systems.

What should I look for when choosing a merchant services provider?

Prioritize fee transparency, fraud protection effectiveness, chargeback management tools, scalability, customer support availability, and integration with your existing ecommerce and billing platforms. For high-risk merchants, also negotiate reserve terms and funding timelines before signing.

.webp)