.png)

A payment processing proposal template is a structured document that outlines pricing models, fees, services, and terms so your business can secure reliable payment processing agreements. For ecommerce and subscription merchants, this document is not optional. It is the foundation of every processor relationship you build. A well-built payment processing proposal template protects you from hidden fees, scope disputes, and mismatched service expectations before you sign anything. Tools like PandaDoc, Proposify, and standard word processors all support the formatting you need, but the structure you put inside the document is what determines your outcome.

What does a payment processing proposal template include?

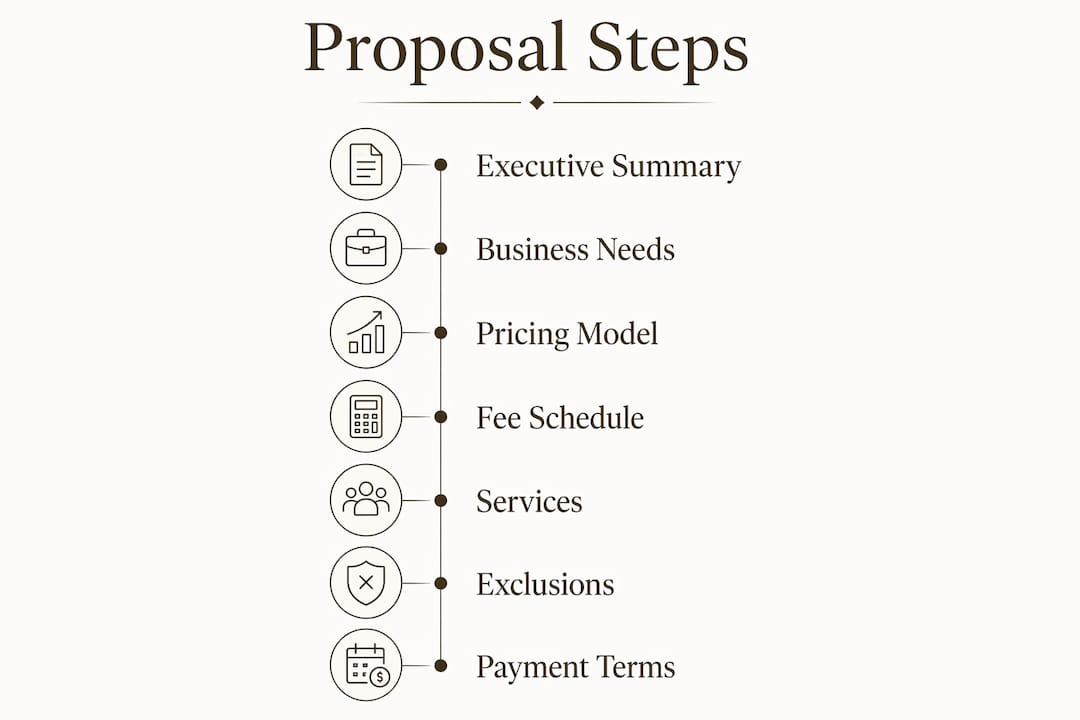

Effective payment processing proposals must include at least 7 critical components to deliver transparency and relevance. Each component serves a specific protective function for your business.

Executive summary. This section states your business model, processing volume, and primary goals in two to three sentences. It tells the processor exactly who you are and what you need.

Business needs context. A proposal is not a sales pitch. It is a record of shared understanding, which makes the “understanding of the brief” section the most critical element for success. State your transaction types, average ticket size, and any high-risk factors upfront.

Transparent pricing model. Processors commonly offer three pricing models: flat-rate, interchange-plus, and subscription-based. Each carries a distinct cost structure.

| Pricing Model | Structure | Best For |

|---|---|---|

| Flat-rate | Fixed percentage per transaction (e.g., 2.6% + $0.10) | Low-volume or new merchants |

| Interchange-plus | Card network cost plus defined processor markup | Mid-to-high volume merchants |

| Subscription-based | Flat monthly fee plus small per-transaction charge | High-volume subscription businesses |

Detailed fee schedule. List every fee line by line: transaction fees, gateway fees, PCI compliance fees, batch fees, chargeback fees, and monthly minimums. Bundled “service fees” often hide higher-than-average markups. A line-item breakdown exposes the true cost structure before you commit.

Services and features. Specify gateway integration options, POS compatibility, mobile processing support, and security compliance certifications. For ecommerce merchants, PCI DSS compliance, tokenization, and end-to-end encryption are non-negotiable inclusions.

Exclusions list. Clear exclusions prevent scope creep and eliminate “I thought it was included” disputes. Name every service or cost that falls outside the agreement.

Payment terms and acceptance section. Include specific deposit amounts, milestone payments, and final payment terms. Add a signature block with date fields for both parties.

Pro Tip: Transparency in fee items is the only way to make valid apples-to-apples comparisons between competing payment processors. Never accept a proposal that groups fees under a single line item.

How to customize your proposal for ecommerce and subscriptions

A generic payment services proposal fails ecommerce and subscription merchants. Your business model has specific needs that a standard template does not address by default.

Subscription-based pricing models can reduce costs significantly for high-volume businesses by avoiding percentage-based volume markups. If you run a subscription business, your proposal must reflect recurring billing cycles, retry logic for failed payments, and dunning management capabilities.

Customize your payment processing plan with these specifics:

- Transaction volume and average ticket size. State your monthly processing volume and average order value. These numbers directly affect which pricing model saves you money.

- Ecommerce platform integrations. Name the platforms you use: Shopify, WooCommerce, BigCommerce, or a custom API. Confirm the processor supports each one.

- Subscription billing cycles. Specify weekly, monthly, or annual billing. Include trial period handling and upgrade or downgrade scenarios.

- Recurring payment authorization. Address how the processor handles stored credentials and card-on-file transactions under network rules.

- Fraud prevention tools. List required tools: AVS checks, CVV verification, 3D Secure 2.0, and velocity filters.

- Chargeback thresholds. State your current chargeback ratio and ask the processor to confirm their threshold before termination.

- 24/7 support SLA. Ecommerce runs around the clock. Your service level agreement must reflect that with guaranteed response times.

Pro Tip: Negotiate your per-transaction fee based on projected monthly volume. Processors routinely offer lower rates at $50,000 or $100,000 monthly thresholds. Put the volume commitment and the corresponding rate in writing inside the proposal.

How to write and structure your payment processing proposal step by step

A clear sequence produces a proposal that processors approve faster and that protects you longer. Follow these steps from draft to final document.

-

Define your business needs clearly. The “understanding of the brief” is the most important proposal section, showing attentiveness and readiness. Write two to three sentences describing your business model, processing history, and primary pain points.

-

Choose and document your preferred pricing model. Reference the three models from the comparison table above. State which model you are requesting and why it fits your volume.

-

Build your fee schedule line by line. Create a table with every fee type in its own row. Leave no fee grouped or bundled.

-

List all services and integrations required. Name every platform, gateway, and security feature your business depends on. Vague descriptions create gaps that processors exploit later.

-

Write your exclusions section. State explicitly what the processor is not responsible for. This protects you from being billed for services you never requested.

-

Set clear payment terms. Specific deposit amounts, milestone payments, and final payment terms decrease future disputes and improve cash flow predictability. Include consequences for late payments.

-

Format for fast review. Consistent bookmarks and schemas speed internal review and allow quick benchmarking of competing offers. Use headers, numbered sections, and tables throughout.

-

Add a signature and acceptance block. Include fields for both parties, the effective date, and a version number.

| Step | Action | Output |

|---|---|---|

| 1 | Define business needs | Two-to-three sentence business context |

| 2 | Select pricing model | Named model with justification |

| 3 | Build fee schedule | Line-item fee table |

| 4 | List services and integrations | Named platforms and certifications |

| 5 | Write exclusions | Explicit out-of-scope list |

| 6 | Set payment terms | Deposit, milestones, final payment |

| 7 | Format consistently | Headers, tables, bookmarks |

| 8 | Add signature block | Dated acceptance section |

Pro Tip: Review every fee line for bundling before you submit. Ask the processor to confirm whether any single line item contains more than one charge. Bundled fees are the most common source of billing disputes in the first 90 days of a processing agreement.

What are the most common mistakes in payment processing proposals?

Most proposal failures trace back to the same small set of errors. Knowing them in advance saves you money and time.

Ambiguity in fee disclosure is a leading cause of disputes between merchants and processors. Hidden service or annual fees buried in fine print create misunderstandings that are expensive to resolve after signing.

Watch for these red flags in any proposal you receive from a processor:

- Fees listed as percentages only, with no dollar example at your average ticket size

- A single “processing fee” line that does not separate interchange from markup

- No mention of PCI compliance fees or chargeback fees

- Vague SLA language like “best effort” instead of specific response time commitments

- Missing exclusions section or a section that reads “all other services excluded” without specifics

- No version number or effective date on the document

Failing to tailor the proposal to your actual business model reduces its credibility. A processor reviewing a generic payment processing agreement with no transaction volume data has no basis for accurate underwriting. That delays approval and often results in less favorable terms.

Pro Tip: Have a financial advisor or attorney review the fee schedule and exclusions section before you sign. A one-hour review fee is far less than the cost of a disputed charge buried in a 24-month processing contract.

Key takeaways

A complete payment processing proposal template must include transparent fee schedules, a clear exclusions list, and pricing model details tailored to your ecommerce or subscription business model.

| Point | Details |

|---|---|

| Seven core components | Every proposal needs an executive summary, pricing model, fee schedule, services list, exclusions, payment terms, and signature block. |

| Pricing model selection | Choose flat-rate, interchange-plus, or subscription-based pricing based on your monthly volume and transaction type. |

| Ecommerce customization | Name your platforms, billing cycles, fraud tools, and chargeback thresholds explicitly to avoid gaps in coverage. |

| Exclusions protect you | A clear exclusions list prevents scope disputes and eliminates unexpected charges after signing. |

| Format for fast approval | Consistent headers, tables, and numbered sections speed processor review and benchmarking. |

Why I treat proposals as legal protection, not paperwork

Most business owners treat a payment processing proposal as a formality. Sign it, get processing, move on. That mindset costs real money.

The proposals I have seen cause the most damage share one trait: they look complete but leave fees undefined. A processor can charge a “regulatory compliance fee” or an “account maintenance fee” every month if those terms are not explicitly excluded. The merchant never questioned it because the proposal did not mention it. That is not an accident on the processor’s part.

The exclusions section is the most underused tool in any payment processing agreement. Writing “all services not listed above are excluded” takes five minutes. It has saved merchants from billing disputes that would have taken months to resolve. Treat that section as seriously as you treat the pricing table.

Proposal automation tools like PandaDoc and Proposify help with formatting and version control, but they do not write your fee schedule for you. The structure they provide is only as good as the specificity you put into it. A well-formatted proposal with vague fee language is still a liability.

View your proposal as a business protection instrument. It documents what you agreed to, what you did not agree to, and what happens if either party fails to deliver. Merchants who approach proposals this way negotiate better rates, avoid surprise fees, and exit bad processor relationships faster when they need to.

— Peter

Davincipay’s payment processing solutions for ecommerce and subscriptions

Davincipay works directly with ecommerce brands, subscription merchants, nutraceutical businesses, and telehealth companies that need reliable, transparent payment processing. We understand the specific challenges these business models face, from chargeback management to recurring billing compliance.

Our payment processing for high-risk businesses covers domestic and international acquiring, fraud prevention, and underwriting support built for complex online merchants. The application process is direct, and fee structures are disclosed line by line before you sign anything. If you are ready to move forward, apply now and our team will review your business needs and match you with the right processing solution.

FAQ

What is a payment processing proposal template?

A payment processing proposal template is a structured document that outlines pricing models, fees, services, and terms between a merchant and a payment processor. It serves as both a negotiation tool and a binding reference for the processing agreement.

What pricing models should a payment proposal template cover?

A complete proposal should address flat-rate, interchange-plus, and subscription-based pricing. Each model carries a different cost structure, and the right choice depends on your monthly transaction volume and average ticket size.

How do I customize a payment processing plan for subscriptions?

Include your billing cycle frequency, retry logic for failed payments, stored credential handling, and dunning management requirements. Subscription merchants should also specify chargeback thresholds and request confirmation that the processor supports recurring authorization under current card network rules.

Why is the exclusions section critical in a payment processing agreement?

Clear exclusions prevent scope creep and eliminate disputes over services or fees that were never agreed upon. Without an explicit exclusions list, processors can add charges that are technically not prohibited by the contract.

What are the most common red flags in a payment services proposal?

Watch for bundled fee lines that group interchange and markup together, missing PCI compliance fee disclosures, vague SLA language, and no effective date or version number on the document. These gaps create billing disputes within the first few months of the agreement.

.webp)