.png)

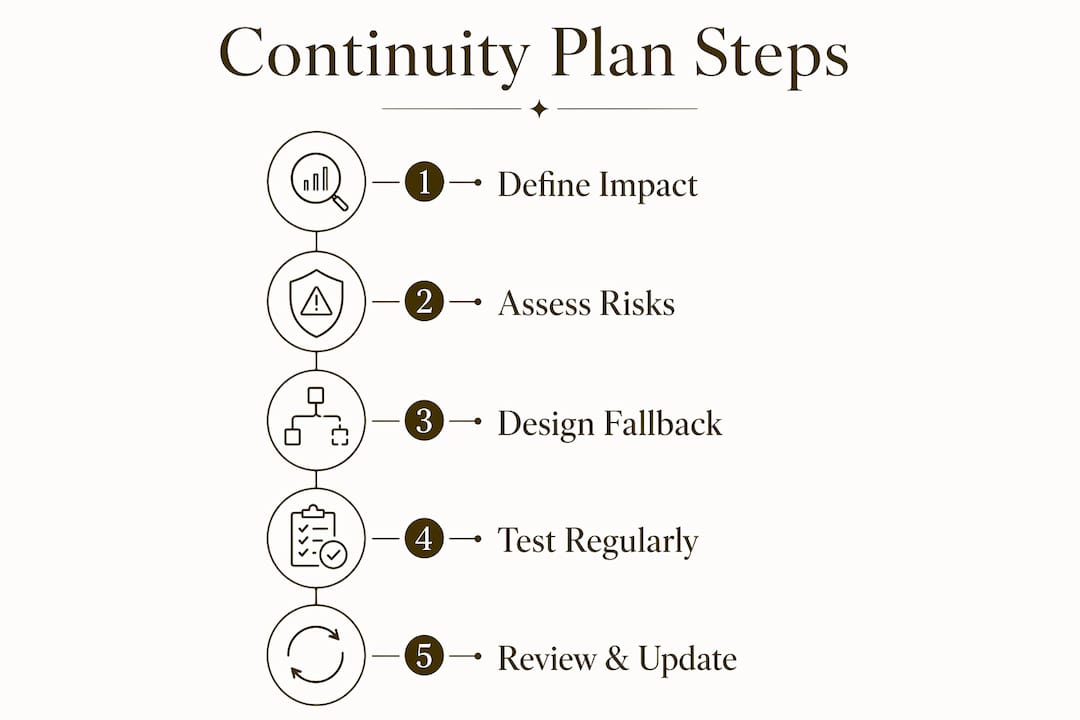

A payment processing continuity plan is a documented strategy that keeps your ecommerce transactions running during unexpected disruptions, from gateway outages to processor failures. Without one, a single point of failure can freeze revenue, delay payroll, and erode customer trust in hours. The industry term for this discipline is operational resilience, and regulators like the UK Financial Conduct Authority (FCA) have formalized it into binding requirements. This guide covers every component your continuity plan for payments needs, from setting impact tolerances to managing vendor risk and testing fallback procedures under real conditions.

What key components make up an effective payment processing continuity plan?

A payment processing continuity plan works when it addresses both technical recovery and financial operations together. Most ecommerce businesses plan for IT outages but ignore what happens to payroll, vendor payments, and cash access when the payment workflow goes dark. That gap is where real damage occurs.

The six core components every plan needs:

Here is how impact tolerances compare to traditional recovery objectives:

MetricRecovery Time Objective (RTO)Impact ToleranceFocusInternal system restorationCustomer harm preventionMeasured byIT teamBusiness outcomeSet byOperationsSenior leadershipRegulatory standardInternal benchmarkFCA-aligned requirementReview frequencyAs neededAnnually or after major changes

Pro Tip: Set your impact tolerances before you design your fallback procedures. If you do not know how much downtime is acceptable, you cannot build the right backup systems to stay within that limit.

The FCA operational resilience framework treats payment continuity as delivering important business services within predefined impact tolerances during severe but plausible disruptions. Even if you are not a regulated UK firm, this framework is the clearest public standard available for building a credible plan.

How to implement payment processing continuity including vendor and counterparty risk management

Implementation is where most plans stall. Businesses document a plan, file it, and never operationalize it. The following steps move your plan from paper to practice.

Pro Tip: Do not wait for a full outage to test your fallback gateway. Run a small volume of live transactions through your backup processor every month. This confirms the integration works and keeps the relationship active with the acquiring bank.

Integrating vendor risks into a formal risk register, with quarterly review cycles, is the single most underused practice in ecommerce payment risk management. Most merchants treat their payment processor like a utility. The ones who have experienced a sudden processor termination know exactly why that assumption is dangerous.

What are best practices for testing and maintaining your payment continuity plan?

Testing is the proof that your plan works. Documentation without testing is just a hypothesis.

Test TypeFrequencyParticipantsPass CriteriaEnd-to-end scenario testTwice per yearIT, payments, financeAll services restored within impact toleranceTabletop exerciseQuarterlyLeadership, operationsClear escalation and decision paths confirmedFallback gateway live testMonthlyPayments teamSuccessful transaction processing on backupManual workaround drillAnnuallyCustomer service, financeStaff complete procedures without documentation gaps

The FCA’s operational resilience requirements push firms to embed this discipline culturally, not just as a compliance checkbox. For ecommerce businesses, that means testing becomes a regular operational rhythm, not a one-time event.

How to recover quickly and communicate effectively during a payment disruption

Speed and clarity define how much damage a payment disruption actually causes. A well-executed response can contain the incident. A poor one turns a two-hour outage into a two-week reputation problem.

After the incident, conduct a formal review within five business days. Identify what triggered the disruption, which parts of your plan worked, and which gaps need to be closed. Update your risk register, adjust your impact tolerances if needed, and schedule a follow-up test of any procedures that failed.

Key takeaways

A payment processing continuity plan requires impact tolerances, active vendor risk management, and end-to-end scenario testing to protect revenue and customer trust during disruptions.

PointDetailsDefine impact tolerances firstSet harm-based thresholds before building fallback systems so your recovery targets match real customer risk.Treat payment processors as active risksAdd acquirers and gateways to your risk register and review them quarterly, not just when problems arise.Test end-to-end, not just ITInclude third-party vendors like gateways and cloud providers in every scenario test to validate true service resilience.Secure financial liquidity in advanceMaintain a reserve account or credit line covering at least two weeks of payroll and vendor obligations.Communicate fast and honestlyPost a customer status update within the first hour of a disruption to contain reputational damage.

Why most payment continuity plans fail before they are ever tested

The honest observation from working with high-risk ecommerce merchants is this: most payment continuity plans are IT recovery plans wearing a business continuity label. They document how to restore a server. They do not document how to pay your team, communicate with your customers, or keep subscriptions billing when your primary processor goes dark.

The shift from IT recovery to true operational resilience is not subtle. It requires you to ask a different question. Instead of “how fast can we restore the system?”, ask “how long can our customers and our business tolerate this disruption?” That question, the one the FCA built its entire operational resilience framework around, forces you to think about harm, not just uptime.

The other failure I see consistently is treating financial counterparties as background infrastructure. Merchants spend weeks vetting a new fulfillment partner but never formally review their payment processor’s financial health or contract terms. Then the processor terminates their account with 30 days notice, and there is no fallback in place. Quarterly counterparty reviews are not bureaucratic overhead. They are the mechanism that keeps your fallback options current.

Post-pandemic, the bar for payment system reliability has moved. Customers expect checkout to work. They do not factor in your vendor’s outage. They factor in whether your store worked when they tried to buy. That expectation is permanent, and the merchants who treat continuity planning as a competitive advantage, rather than a compliance task, are the ones who retain customers through incidents that would otherwise cost them permanently.

How Davincipay supports your payment continuity strategy

Davincipay is built specifically for ecommerce businesses that cannot afford payment gaps. Whether you run a nutraceutical brand, a telehealth platform, or a high-volume subscription business, Davincipay provides access to multiple domestic and international acquiring relationships so you always have a live fallback option. Real-time monitoring, chargeback mitigation, and fraud prevention tools are built into the platform, giving you the visibility your payment risk management strategy requires. If your current setup depends on a single processor with no backup, that is a gap Davincipay can close. Apply now and get your payment continuity infrastructure in place before the next disruption finds you unprepared.

FAQ

What is a payment processing continuity plan?

A payment processing continuity plan is a documented strategy that keeps ecommerce transactions running during disruptions by defining fallback procedures, impact tolerances, and financial contingency measures. It covers both technical recovery and financial operations, including payroll and vendor payments.

How often should you test your payment continuity plan?

End-to-end scenario tests should run at least twice per year, with monthly live tests of fallback gateways and quarterly tabletop exercises. Impact tolerances should be reviewed annually or after any material change to your business or payment stack.

What are impact tolerances in payment continuity planning?

Impact tolerances are harm-based thresholds that define the maximum acceptable disruption time before customer harm becomes intolerable. They differ from internal recovery time objectives because they measure business outcomes and consumer harm, not just system restoration speed.

Why should payment processors be included in vendor risk management?

Failure of a financial partner can disrupt operations and stall payment processing exactly when stability is most critical. Quarterly reviews of payment processors and acquiring banks keep your fallback options current and your risk register accurate.

What should you communicate to customers during a payment outage?

Post a specific status update on your website and send a direct email to affected customers within the first hour. State what is affected, what you are doing to fix it, and when you expect resolution. Specific, honest communication reduces customer anxiety and protects long-term trust.

Recommended

- DavinciPay | Payment Processing For High-Risk Businesses

- Apply Now | DavinciPay

- DavinciPay for Telehealth | Payment Processing

- DavinciPay for Supplements | Payment Processing

.webp)