.png)

Payment industry certification is the formal process of validating that professionals, merchants, and service providers meet globally recognized security and compliance standards for handling payment card data. The most critical framework in this space is PCI DSS, governed by the PCI Security Standards Council (PCI SSC), but certifications like the Certified Payments Professional (CPP) from the Electronic Transactions Association (ETA), the Certified Payments Card Industry Professional (PCIP), and the Certified Community Payments Manager (CCPM) also define the professional side of the field. Understanding payment industry standards is not optional for anyone operating in payments. It directly affects your ability to process transactions, win contracts, and avoid financial penalties that can reach into the millions.

What are the main payment industry certifications and their scopes?

Payment certifications fall into two distinct categories: organizational compliance frameworks and individual professional credentials. Confusing the two is one of the most common mistakes payment professionals make.

Organizational compliance frameworks validate that a business or service provider meets specific security controls for handling cardholder data. PCI DSS is the dominant standard here. PCI DSS, SOC 2, and ISO 27001 each serve different assurance purposes. PCI DSS is payment-data specific and scope-sensitive, while SOC 2 covers trust service criteria broadly and ISO 27001 governs an information security management system. None of these are substitutes for each other when card data is in scope.

Individual professional credentials validate a person’s knowledge of payment systems, compliance requirements, and industry operations. The ETA CPP is the most widely recognized credential for payment professionals, covering sales, operations, and compliance. The PCIP, offered through the PCI SSC, focuses specifically on PCI DSS knowledge. The CCPM targets community banking professionals managing payment programs.

CertificationTypePrimary FocusTypical HolderPCI DSSOrganizational complianceCardholder data securityMerchants, service providersSOC 2Organizational complianceBroad security controlsSaaS and cloud providersISO 27001Organizational complianceInformation security managementEnterprises, fintechsETA CPPIndividual professionalPayments industry knowledgeSales, ops, compliance rolesPCIPIndividual professionalPCI DSS expertiseSecurity and compliance staffCCPMIndividual professionalCommunity payment managementBanking professionals

Pro Tip: If you work at a payment gateway or ISO, pursue the ETA CPP for career credibility and the PCIP for technical depth. They complement each other and signal to employers that you understand both the business and security dimensions of payments.

How is PCI DSS compliance validated in the payment industry?

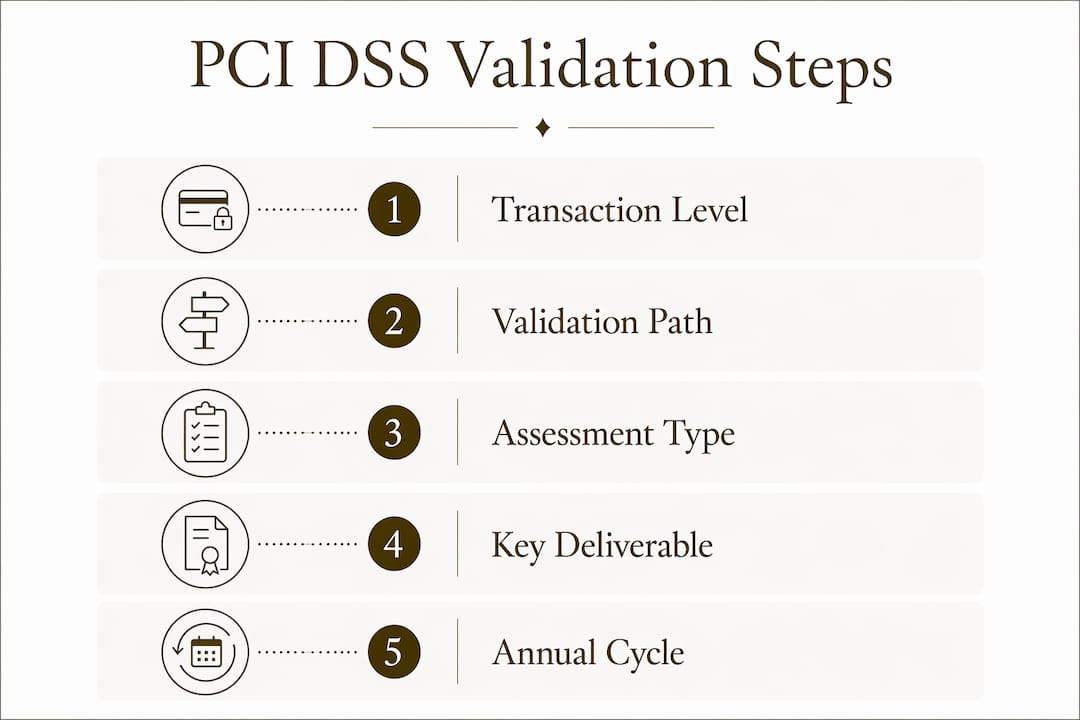

PCI DSS validation is not a single process. The path you take depends entirely on your transaction volume and how your systems interact with cardholder data.

Merchants are segmented into four levels based on annual Visa or Mastercard transaction volume. Level 1 merchants process more than 6 million transactions annually and must undergo a full audit conducted by a Qualified Security Assessor (QSA), producing a Report on Compliance (ROC). Levels 2 through 4 merchants use Self-Assessment Questionnaires (SAQ), which range from 22 to 329 questions depending on the payment environment. SAQ complexity reflects how many systems touch cardholder data, which is why reducing your scope through tokenization or point-to-point encryption is a practical compliance strategy.

The cost and time differences between these paths are significant. Level 1 assessments cost between $30,000 and $200,000 and take 6 to 12 months to complete. SAQ paths cost between $1,000 and $40,000 and typically take 3 to 6 months. These figures matter when budgeting for compliance programs, especially for high-growth merchants moving between levels.

The document that actually proves your compliance to the outside world is the Attestation of Compliance (AOC). The AOC is the document shared with acquiring banks and business partners to confirm compliance status. The ROC and SAQ are internal working documents. Sharing a ROC with a client instead of an AOC is a common error that signals inexperience.

Merchant levelAnnual transactionsValidation methodKey deliverableLevel 1Over 6 millionQSA-led ROC auditReport on Compliance + AOCLevel 21 to 6 millionSAQ or QSA auditSAQ + AOCLevel 320,000 to 1 million (e-commerce)SAQSAQ + AOCLevel 4Under 20,000 (e-commerce)SAQSAQ + AOC

Beyond the annual assessment, quarterly external vulnerability scans and annual penetration testing are mandatory for all applicable entities. Penetration testing must cover all in-scope infrastructure and be conducted by qualified personnel. These are not optional add-ons. They are core requirements that many smaller merchants overlook until an acquiring bank flags the gap.

Key compliance artifacts you need to manage:

Why payment certification is a continuous process, not a one-time event

The phrase “PCI certified” is technically incorrect, and using it in a professional context undermines your credibility. PCI compliance is a process, not a certificate. Organizations achieve a state of compliance that must be maintained and revalidated annually. A clean assessment last year means nothing if controls have drifted since then.

“Falling out of compliance between audits means non-compliance despite prior clean assessments.” — PCI DSS compliance guidance

The consequences of non-compliance are concrete. Data breaches cost an average of $4.44 million globally, and that figure does not include contractual penalties from card brands like Visa and Mastercard. Acquirers can impose monthly fines, increase reserve requirements, or terminate processing agreements entirely. For high-risk merchants in sectors like nutraceuticals or telehealth payment processing, losing processing access is an existential threat, not just a financial inconvenience.

Continuous compliance requires more than annual assessments. You need to monitor security controls between audits, track changes to your cardholder data environment (CDE), and manage vendor compliance as part of your own program. Businesses must maintain a list of service providers and verify their compliance status, tracking AOC expiry dates. If a vendor’s AOC lapses and they handle card data on your behalf, that gap becomes your compliance problem.

Common pitfalls that break continuous compliance:

Pro Tip: Build a compliance calendar with hard deadlines for AOC renewals, ASV scans, and penetration tests. Set reminders 60 days before each deadline. This single habit prevents most of the avoidable compliance failures we see in payment organizations.

How certifications enhance credibility and compliance for payment professionals

Certifications do more than satisfy regulatory checkboxes. They function as trust signals in every commercial relationship you have in the payments ecosystem.

Here is how certifications create tangible value for payment professionals and organizations:

Selecting the right certification depends on your role. If you manage payment operations or sales, the ETA CPP is the most recognized credential. If you work in security or compliance, the PCIP provides the technical depth that hiring managers in payment organizations specifically look for. If your organization processes card data at any volume, PCI DSS compliance is not a choice. It is a contractual requirement from your acquiring bank.

Key takeaways

Payment industry certifications divide into organizational compliance frameworks like PCI DSS and individual professional credentials like the ETA CPP, and both require active maintenance to remain valid and credible.

PointDetailsPCI DSS is compliance, not certificationThe correct term is “attestation of compliance.” No organization is ever “PCI certified.”Validation path depends on volumeLevel 1 merchants need a QSA-led ROC; lower-volume merchants use SAQs ranging from 22 to 329 questions.AOC is the only external proofShare the AOC with banks and partners, not the ROC or SAQ, to demonstrate compliance status.Compliance requires continuous effortAnnual assessments, quarterly scans, and vendor AOC tracking are all mandatory, not optional.Certifications drive commercial valueETA CPP and PCIP credentials accelerate hiring, contract wins, and vendor onboarding in payments.

What I’ve learned about payment certifications after years in the industry

The most persistent problem I see is organizations treating PCI DSS as an annual checkbox rather than an ongoing operational discipline. They pass their assessment in Q1, make no changes to their security program, and then wonder why they fail a spot check or suffer a breach in Q4. The assessment proves you were compliant on a specific date. It does not guarantee anything after that.

The second issue is scope confusion. Organizations routinely underestimate their cardholder data environment. They exclude systems that technically touch card data because including them would increase assessment complexity. This is a short-term thinking trap. When a breach occurs, the forensic investigation will find every system that touched card data, regardless of what your scope documentation says.

On the professional credential side, I think the ETA CPP is undervalued by employers who have not worked with credentialed staff before. Once you have a team where multiple people hold the CPP, the quality of compliance conversations with acquirers and card brands changes noticeably. You spend less time explaining basics and more time solving real problems.

My practical advice: verify the scope, assessment method, and AOC validity of every vendor you onboard. Do not accept a compliance logo on a website as proof of anything. Request the actual AOC, check the assessment date, and confirm the scope covers the services you are purchasing. This one practice will save you from inheriting someone else’s compliance gap.

How Davincipay supports your compliance journey

Davincipay works with high-risk merchants, telehealth providers, nutraceutical brands, and supplement businesses that need payment processing built around compliance from the start. Our onboarding process is designed with PCI DSS standards in mind, so you are not scrambling to meet requirements after you start processing. We connect you with acquiring relationships, payment gateways, and underwriting support that account for your compliance posture. Whether you are navigating your first SAQ or managing a Level 1 audit cycle, Davincipay gives you the infrastructure and guidance to process payments securely. Start your application and work with a team that understands what compliance actually requires in your sector.

FAQ

What does “payment industry certification” mean?

Payment industry certification refers to both organizational compliance validations like PCI DSS and individual professional credentials like the ETA CPP or PCIP. These standards confirm that businesses and professionals meet recognized security and operational requirements for handling payment transactions.

Is there such a thing as “PCI certification”?

No. PCI DSS does not issue a certificate. The correct term is attestation of compliance (AOC), which is the document that proves a merchant or service provider met PCI DSS requirements during a specific assessment period.

What is the difference between an SAQ and a ROC?

A Self-Assessment Questionnaire (SAQ) is a self-reported compliance tool used by lower-volume merchants, ranging from 22 to 329 questions. A Report on Compliance (ROC) is a formal audit document produced by a Qualified Security Assessor (QSA) and required for Level 1 merchants processing over 6 million transactions annually.

How often must PCI DSS compliance be revalidated?

PCI DSS compliance requires annual revalidation through an SAQ or QSA audit, plus quarterly external vulnerability scans and annual penetration testing. Compliance is a continuous state, not a one-time achievement.

Which payment certification is best for a compliance professional?

The PCIP from the PCI SSC is the most targeted credential for compliance professionals working directly with PCI DSS requirements. The ETA CPP is broader and better suited for professionals managing payment operations, sales, or risk management across the full payments ecosystem.

.webp)