.png)

A multi-merchant payment platform is software that connects multiple merchant accounts to a single payment gateway, letting businesses process, route, and reconcile transactions across several vendors or locations from one interface. The industry term you will see in technical documentation is “multi-merchant payment gateway,” and it covers everything from transaction splitting to vendor-level reporting. Platforms like Corefy and Boulevard have built their core infrastructure around this model, and payment service providers (PSPs) increasingly offer it as a standard feature. If you manage more than one vendor, brand, or business location, understanding this architecture is not optional. It is the foundation of efficient payment operations.

What is a multi-merchant payment platform, exactly?

A multi-merchant payment gateway enables managing multiple merchant accounts through one gateway interface. That single sentence captures the core function, but the operational implications run deeper than the definition suggests.

Each merchant account in the system belongs to a separate legal or financial entity. The platform connects all of them to one acquiring bank relationship or a network of acquiring banks, depending on the setup. Transactions flow in, get routed to the correct merchant account, and settle directly into that merchant’s bank account. No manual splitting. No shared settlement pools that require reconciliation after the fact.

This structure matters most for businesses that operate across multiple revenue streams. Think of a salon suite operator with 12 independent stylists, a marketplace with 50 vendors, or a telehealth company with multiple licensed practitioners billing under separate tax IDs. Each entity needs its own financial record. A multi-merchant platform delivers that without requiring each vendor to manage a completely separate payment stack.

The broader payment ecosystem connects to this model through payment service providers, acquiring banks, and payment gateways. PSPs like Stripe and Adyen offer multi-merchant functionality as part of their platform products. Acquiring banks underwrite each merchant account individually. The gateway sits in the middle, routing transactions and enforcing the rules of each account.

How does a multi-merchant payment platform work?

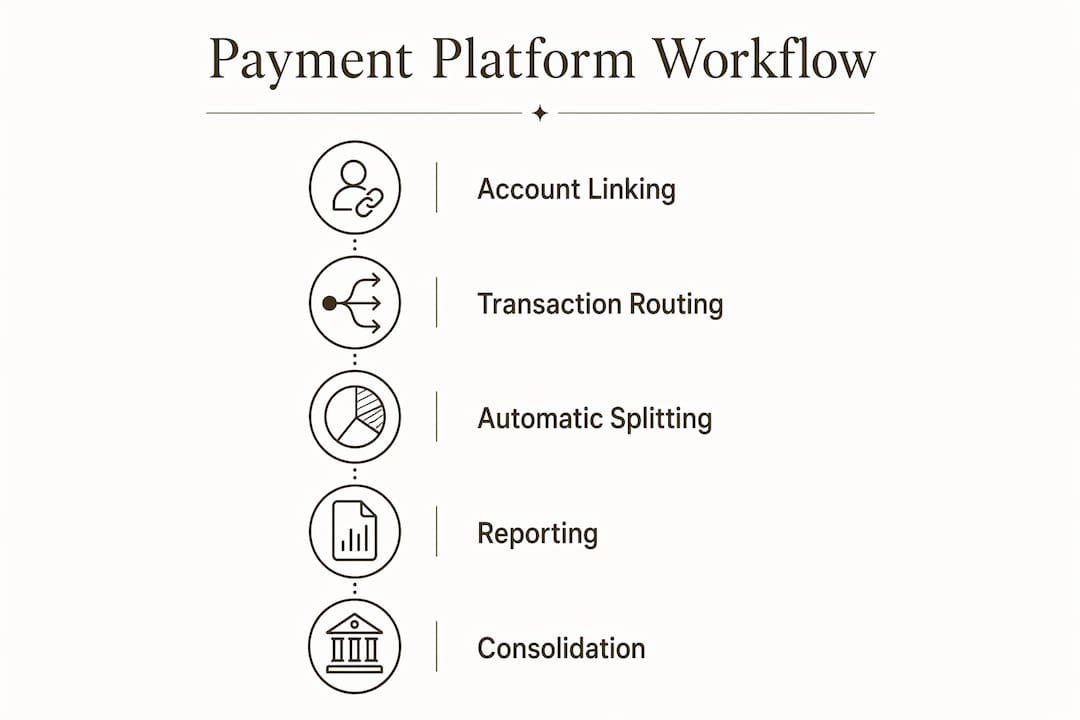

The technical architecture of a multi-merchant payment system rests on three pillars: account linking, transaction routing, and security infrastructure.

Account linking is the starting point. Each vendor or merchant registers a separate merchant account, goes through underwriting, and gets approved by an acquiring bank. The platform then links all approved accounts to one gateway. From the operator’s view, it looks like a single dashboard. From the acquiring bank’s view, each account is independent.

Transaction routing is where the platform earns its value. When a customer pays at checkout, the platform reads the transaction data, identifies which merchant or vendor the payment belongs to, and routes it to the correct account. Sales split automatically with a single card swipe, and fees apply per merchant portion. This removes the manual work of splitting revenue after settlement.

Security infrastructure is non-negotiable. Modern payment platforms use API-first architectures, microservices, and tokenization to deliver high availability, fault tolerance, and reduced PCI compliance scope. Tokenization replaces sensitive card data with a non-sensitive token, so the actual card number never sits in your system. That reduction in compliance scope translates directly to lower audit costs and reduced liability.

Key technical features to look for in any multi-merchant system:

- API-first design: Lets you connect the platform to your existing POS, ERP, or booking software without rebuilding your stack

- Tokenization: Moves card data out of your environment and into a secure vault

- PCI DSS compliance tools: Reduces the scope of your annual compliance audit

- Fault-tolerant routing: Keeps transactions processing even if one acquiring bank connection goes down

- Merchant-level reporting: Gives each vendor access to their own transaction data without exposing other merchants’ records

Pro Tip: Before signing with any multi-merchant platform, ask specifically whether their tokenization covers all payment methods you accept. Some platforms tokenize card payments but leave ACH or digital wallet data in a less secure environment.

One important limitation: Apple Pay and Google Pay often have restricted support in multi-merchant setups due to routing restrictions and terminal configurations. Verify digital wallet compatibility before you commit to a platform migration.

What are the main benefits of a multi-merchant platform?

The operational advantages of multi-vendor payment solutions are concrete and measurable. Here is what changes when you consolidate onto one platform.

Automatic transaction splitting simplifies vendor payouts and cuts operational overhead. Instead of collecting revenue in one account and manually distributing it, the platform handles distribution at the moment of sale. Each vendor gets paid directly. Your finance team stops spending hours on reconciliation.

Reporting improves significantly. Each merchant account generates its own transaction history, settlement reports, and fee statements. You get a consolidated view at the operator level and a granular view at the vendor level. That combination makes month-end close faster and audits cleaner.

Cost consolidation is another real advantage. Running separate payment stacks for each vendor, each with its own gateway subscription, PCI compliance program, and support contract, adds up fast. A single multi-merchant platform typically carries one gateway fee, one compliance program, and one support relationship. The savings scale with the number of vendors you manage.

Security and compliance benefits are equally significant. End-to-end encryption, tokenization, multi-factor authentication, and fraud detection are standard features in modern platforms. Each vendor benefits from enterprise-grade security without having to build or buy it independently.

The summary of core benefits:

- Direct vendor deposits with no manual distribution

- Consolidated reporting with merchant-level drill-down

- Single compliance program covering all accounts

- Reduced gateway and processing fees through volume consolidation

- Fraud detection applied uniformly across all merchant accounts

Multi-merchant platform vs. alternative solutions

Choosing the right architecture depends on your business model, vendor count, and technical resources. Three main options exist: a unified multi-merchant platform, a multi-gateway strategy, and multi-merchant terminals.

| Solution | Best For | Key Advantage | Key Limitation |

|---|---|---|---|

| Multi-merchant platform | Marketplaces, salons, shared spaces | Unified dashboard, automatic splitting | Vendor underwriting required per account |

| Multi-gateway setup | Large enterprises needing redundancy | Flexibility, failover routing | Higher integration complexity and maintenance cost |

| Multi-merchant terminal | Retail locations with shared hardware | Low hardware cost, simple setup | Limited reporting, restricted digital wallet support |

A multi-gateway strategy uses several payment gateways simultaneously. Businesses choose this for redundancy or to access different acquiring relationships in different regions. The tradeoff is real: multiple gateways add integration complexity and higher maintenance overhead compared to a unified multi-merchant platform. You gain flexibility but pay for it in engineering time and ongoing management.

Multi-merchant credit card terminals let multiple independent businesses share one card reader while keeping accounts and revenue separate. This works well in a small shared retail space where hardware cost matters more than reporting depth. The limitation is that terminal-based systems offer minimal analytics and frequently restrict digital wallet payments in multi-merchant routing configurations.

The unified multi-merchant platform wins on operational efficiency for most businesses managing more than five vendors. The multi-gateway approach makes sense for enterprises with dedicated engineering teams and complex international acquiring needs. Terminals are a fit for simple, low-volume shared spaces.

Practical applications across industries

Multi-merchant payment systems solve real problems in specific industries. Here are four scenarios where the architecture delivers clear value.

-

Salon suites and shared service spaces: A suite operator hosts 15 independent stylists. Each stylist has their own merchant account linked to the operator’s platform. Clients pay at a shared terminal or through an app. Funds route directly to each stylist’s account. Boulevard’s multi-merchant account model is built precisely for this use case, with staff merchant accounts tied to individual service providers.

-

Online marketplaces: A marketplace with dozens of vendors needs to collect payment from buyers and distribute funds to sellers without holding money in a shared pool. A multi-merchant platform handles this at the transaction level, routing each vendor’s portion of a sale directly to their account at settlement.

-

Telehealth platforms: A telehealth company with multiple licensed practitioners billing under separate NPI numbers needs each provider’s revenue tracked independently for compliance and tax purposes. A multi-merchant setup gives each provider their own merchant account while the operator maintains a consolidated view. Davincipay’s telehealth payment processing infrastructure is designed for exactly this kind of regulated, multi-provider environment.

-

Nutraceutical and supplement brands with multiple product lines: Brands operating distinct product lines under separate legal entities use multi-merchant platforms to keep revenue, chargebacks, and compliance records separate. This protects one product line from the chargeback history of another.

Pro Tip: When onboarding vendors to a multi-merchant platform, collect all underwriting documents upfront. Merchant accounts can be declined or suspended based on credit history, chargeback ratios, or tax liens. A clean onboarding process prevents delays that disrupt your vendors’ ability to accept payments.

For businesses exploring multi-jurisdiction payment structures, the multi-merchant model also provides a foundation for managing cross-border acquiring relationships under one operational roof.

Key takeaways

A multi-merchant payment platform is the most operationally efficient solution for businesses managing five or more vendors, combining automatic transaction splitting, merchant-level reporting, and consolidated compliance under one gateway.

| Point | Details |

|---|---|

| Core function | Links multiple merchant accounts to one gateway for automatic routing and splitting. |

| Security standard | Tokenization and end-to-end encryption reduce PCI scope and fraud exposure for all vendors. |

| Digital wallet limits | Apple Pay and Google Pay often lack support in multi-merchant setups; verify before migrating. |

| Best use cases | Salon suites, online marketplaces, telehealth platforms, and multi-brand ecommerce operations. |

| Vendor onboarding risk | Each merchant account requires individual underwriting; bad credit or high chargebacks can cause denial. |

What i’ve learned after years of working with multi-merchant payment infrastructure

Most business owners approach multi-merchant platforms as a billing convenience. They want to stop manually splitting revenue. That is a valid starting point, but it undersells the real value and causes people to make poor platform choices.

The decision that matters most is API capability. API-first payment platforms let you update or swap components without service interruption. That flexibility is not a technical luxury. It is a business continuity requirement. I have seen operators locked into platforms with rigid integrations that could not accommodate a new POS system or a new acquiring bank relationship. The cost of switching mid-operation is brutal.

The second thing most people underestimate is the underwriting layer. Every merchant account in your system requires individual approval. If one of your vendors has a history of excessive chargebacks or a tax lien, their account gets declined. That is not a platform failure. That is the acquiring bank doing its job. Build your onboarding process around this reality. Collect financial documentation before you promise a vendor they are live.

On digital wallets: the restriction on Apple Pay and Google Pay in multi-merchant environments is a real operational gap, not a minor footnote. If your customer base skews toward mobile payments, this matters. Ask every platform you evaluate for a written answer on digital wallet support in multi-merchant routing before you sign anything.

The platforms that serve high-risk and complex businesses best are the ones that combine strong acquiring relationships with flexible API architecture. Generic platforms built for low-risk retail often cannot handle the compliance requirements, chargeback management, or international acquiring needs that come with regulated industries. Choose a platform that was built for your complexity, not one that tolerates it.

— Peter

How Davincipay supports multi-merchant payment operations

Davincipay specializes in payment processing for businesses that standard platforms turn away. If you operate a marketplace, a multi-provider telehealth service, a nutraceutical brand, or any business managing multiple vendor accounts, Davincipay’s infrastructure is built for that complexity.

Davincipay provides domestic and international acquiring relationships, fraud prevention tools, chargeback mitigation, and underwriting support across high-risk and regulated sectors. The platform is designed to handle the compliance requirements, account structures, and payment routing that multi-vendor businesses actually need. Whether you are processing for supplement brands or managing multiple service providers under one roof, Davincipay delivers the payment infrastructure to keep your operation running. Apply now and get your multi-merchant payment setup moving.

FAQ

What is a multi-merchant payment platform?

A multi-merchant payment platform is software that connects multiple merchant accounts to one payment gateway, enabling automatic transaction routing, splitting, and settlement to individual vendor accounts. It is the standard solution for businesses managing payments across multiple vendors, locations, or service providers.

How does transaction splitting work in multi-merchant systems?

Sales are split automatically at the point of transaction, with each merchant’s portion routed directly to their linked bank account. Fees apply per merchant portion, and no manual distribution is required after settlement.

Do all payment methods work with multi-merchant platforms?

Not always. Apple Pay and Google Pay frequently have limited support in multi-merchant setups due to routing restrictions and terminal configuration requirements. Always verify digital wallet compatibility with your platform before migrating.

What are the risks of setting up merchant accounts for multiple vendors?

Each merchant account requires individual underwriting. Vendors with poor credit history, tax liens, or high chargeback ratios can be declined or suspended by the acquiring bank. Collecting underwriting documents before onboarding prevents delays.

How does a multi-merchant platform differ from a multi-gateway setup?

A multi-merchant platform routes transactions across multiple accounts through one gateway. A multi-gateway setup uses several gateways simultaneously for redundancy or regional flexibility, but adds integration complexity and higher maintenance costs compared to a unified platform.

.webp)