.png)

A merchant payment infrastructure audit is a structured evaluation of your ecommerce payment ecosystem to verify security, compliance, and cost efficiency across every stage of the transaction lifecycle. Most merchants treat audits as a one-time compliance checkbox. The ones who avoid costly surprises treat them as an ongoing operational discipline covering settlement controls, dispute management, AML/KYC obligations, and vendor governance. Frameworks like PCI DSS and SOC 2 define the minimum standard. Your audit should go further, examining processor fees, contract terms, and third-party risk alongside technical controls.

What does a merchant payment infrastructure audit actually cover?

A full payment lifecycle audit covers settlement and reconciliation, dispute and chargeback management, AML/KYC/CTF compliance, and governance oversight. That scope is broader than most merchants expect. Checking your checkout page for SSL is not an audit. It is one data point in a much larger picture.

The table below maps the core audit domains and what each one requires you to examine.

| Audit domain | What to examine |

|---|---|

| Settlement and reconciliation | Daily batch totals, funding timelines, reconciliation exceptions |

| Dispute and chargeback management | Chargeback ratios, response workflows, evidence documentation |

| AML/KYC/CTF compliance | Customer verification records, transaction monitoring, suspicious activity reports |

| PCI DSS controls | SAQ classification, log protection, script inventory, network segmentation |

| Vendor and third-party governance | Contract audit rights, SOC reports, ongoing monitoring evidence |

| Fee and cost analysis | Interchange pass-through, processor markups, effective rate trends |

Payment infrastructure audits in the US can also include MSB classification and independent BSA/AML program testing under 31 C.F.R. § 1022.210(d)(4). That regulatory layer sits entirely outside PCI DSS. Merchants who process high transaction volumes or operate in regulated categories like telehealth or nutraceuticals face both sets of requirements simultaneously.

Your audit scope also depends on how your payment pages are built. Merchants who fully outsource payment pages to a hosted provider carry a lighter PCI burden than merchants who host any part of the payment flow themselves. That distinction determines which SAQ type applies to you, and the difference in audit workload is significant.

- Settlement controls: Verify that daily settlement totals match your processor reports and bank deposits. Unreconciled differences signal either processing errors or fraud.

- Dispute management: Confirm your team has documented response workflows and that chargeback ratios stay within card network thresholds.

- AML/KYC/CTF: Review customer onboarding records and transaction monitoring logs for completeness and timeliness.

- PCI DSS: Validate your SAQ type, confirm log retention meets requirements, and check that script inventories are current.

- Vendor governance: Confirm that every payment vendor contract includes audit rights and that you collect periodic evidence such as SOC 2 reports.

What do you need before starting a payment processing audit?

Preparation determines whether your audit produces findings you can act on or a stack of incomplete data. Gather these documents before you start.

- Last three months of merchant statements in PDF format

- Current processor and gateway contracts, including fee schedules

- Your most recent PCI DSS SAQ form and any prior assessment reports

- A list of all third-party vendors touching your payment environment

- Log exports from your payment gateway, fraud tools, and any hosted payment pages

Understanding your SAQ classification is the single most important prerequisite. SAQ types vary significantly: SAQ A covers roughly 22 questions for merchants with fully outsourced payment pages, SAQ A-EP covers approximately 191 questions for merchants hosting payment-influencing pages without storing card data, and SAQ D covers 329 or more questions for merchants who store cardholder data. Choosing the wrong SAQ type does not reduce your compliance burden. It just means your audit misses the controls that actually apply to you.

Third-party due diligence starts before onboarding, not after. Vendor management best practices require risk-ranked vendor inventories, contract clauses granting audit rights, and periodic evidence collection such as SOC reports and incident notifications. If a vendor cannot provide a current SOC 2 Type II report, that is a finding before your audit even begins.

Pro Tip: Maintain a centralized script inventory for every JavaScript file loaded on your payment pages. PCI DSS Requirements 6.4.3 and 11.6.1 require SAQ A-EP merchants to authorize each script and monitor for changes weekly. Most merchants discover gaps in this inventory only when an assessor asks for it.

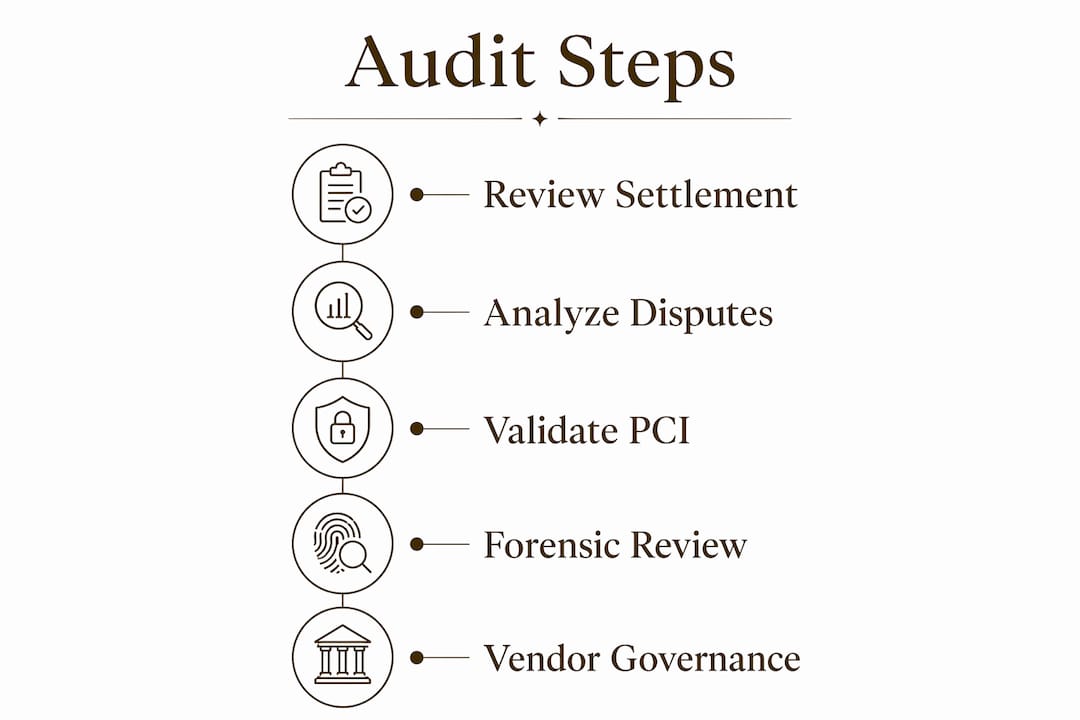

How do you conduct the audit step by step?

A payment system evaluation moves through five distinct phases. Each phase builds on the last. Skipping one creates gaps that surface during assessments or, worse, during an actual incident.

Step 1: Review settlement and reconciliation controls. Pull three months of settlement reports and compare them against your bank statements line by line. Flag any funding delays beyond your contracted settlement window. Reconciliation exceptions that repeat across months point to systemic processing errors, not one-off mistakes.

Step 2: Analyze dispute and chargeback management. Calculate your chargeback ratio for each card network separately. Visa and Mastercard use different thresholds and different monitoring programs. Review your dispute response templates and confirm your team can meet the response deadlines your processor requires.

Step 3: Validate PCI DSS compliance. Confirm your SAQ type matches your actual payment architecture. PCI DSS Requirement 10 mandates that audit logs are protected from unauthorized modification and reviewed regularly using automated tools for anomaly detection. Check that your logs capture the required data fields: user ID, event type, date and time, success or failure, and the originating system.

Step 4: Perform a merchant statement forensic review. A statement audit typically reviews three months of statements and takes 60–90 minutes with prepared PDFs. Build a spreadsheet with rows for each month and columns for transaction volume, total fees paid, and effective rate. Separate pass-through interchange fees from your processor’s markup. Processors often bury margin in non-interchange fees labeled as “service fees” or “network access charges.”

Step 5: Assess vendor governance. Review every active vendor contract for audit right clauses. Third-party oversight requires not just contract rights but documented, ongoing monitoring evidence aligned with risk assessments. Collect the most recent SOC report for each critical vendor and confirm it covers the period relevant to your audit.

The table below compares two common approaches to executing a payment infrastructure analysis.

| Approach | Best for | Limitations |

|---|---|---|

| Internal audit team | Merchants with dedicated compliance staff | Requires deep PCI and AML expertise in-house |

| External QSA or consultant | Merchants without internal compliance resources | Higher cost; requires thorough vendor selection |

Pro Tip: Automate your audit log reviews with a SIEM tool such as Splunk or IBM QRadar. Manual log review fails PCI DSS Requirement 10 because automated anomaly detection is explicitly required, not just recommended.

What are the most common audit pitfalls and how do you fix them?

The most common reason merchants fail a payment processing audit is not a technical gap. It is missing documentation. Assessors and examiners need evidence, not explanations.

- Incomplete script inventories: SAQ A-EP merchants frequently lack a documented list of every script on their payment pages. Feroot Security notes that continuous script monitoring is the hardest operational challenge for these merchants because auditors expect alert history and authorization records, not just a current snapshot.

- Insufficient log retention: PCI DSS requires audit logs to be retained for at least one year, with three months immediately available for forensic analysis. Many teams export logs but store them in formats that lack tamper protection or complete data fields.

- Missing vendor evidence: Contracts with audit rights mean nothing without collected evidence. A SOC 2 report from two years ago does not satisfy current monitoring requirements.

- Point-in-time thinking: A single annual audit does not demonstrate continuous compliance. Assessors look for evidence of ongoing monitoring, not just a clean report from one day of the year.

Verification works in both directions. You need to demonstrate audit evidence to PCI assessors and third-party risk examiners. That means centralized, tamper-protected logs with timestamps, user IDs, and event data. It also means documented remediation steps for every finding, with dates and responsible owners recorded.

Pro Tip: Create a dedicated audit evidence folder updated monthly. Include log exports, vendor SOC reports, script inventory snapshots, and chargeback ratio reports. When an assessor asks for evidence, you pull one folder, not six systems.

Key takeaways

A merchant payment infrastructure audit covers settlement, PCI DSS compliance, fee analysis, and vendor governance, and each area requires documented evidence, not just current controls.

| Point | Details |

|---|---|

| Know your SAQ type | Your PCI DSS SAQ determines your full audit scope; choosing the wrong type leaves real gaps unexamined. |

| Audit logs need protection | Retain logs for one year with three months immediately accessible and use automated tools for review. |

| Script inventories are mandatory | SAQ A-EP merchants must document, authorize, and monitor every payment page script weekly. |

| Statement reviews find hidden fees | A 60–90 minute forensic review of three months of statements separates interchange from processor markups. |

| Vendor evidence must be ongoing | Collect SOC reports and monitoring records continuously, not just at contract signing. |

Why audits are a business capability, not a compliance event

Most merchants I work with treat a payment infrastructure audit as something that happens to them, usually triggered by a processor request or a failed assessment. That framing costs them money and exposes them to risk they could have caught months earlier.

The merchants who handle audits well build them into their operating rhythm. They maintain live script inventories. They review merchant statements quarterly, not annually. They collect vendor SOC reports on a schedule tied to contract renewal dates. When an assessor shows up, they are not scrambling. They pull a folder.

The shift I have seen accelerate recently is QSA enforcement around script monitoring and log review rigor. Assessors who accepted manual log reviews two years ago now require evidence of automated anomaly detection. SAQ A-EP merchants who assumed outsourced payment processing eliminated their compliance scope are learning that hosted payment pages keep them firmly in scope for Requirements 6.4.3 and 11.6.1.

The other trap I see regularly is vendor governance that exists on paper but not in practice. A contract clause granting audit rights does nothing if you never exercise it or collect monitoring evidence. Third-party risk examiners are specifically looking for the gap between what your contracts say and what your evidence files show.

Treat your payment infrastructure audit as a structural business capability. Build the documentation habits, the monitoring tools, and the evidence collection processes before you need them. The merchants who do this consistently face fewer surprises, lower fraud losses, and faster approvals when they need new acquiring relationships.

— Peter

How Davincipay supports audit-ready payment infrastructure

Davincipay specializes in payment processing for high-risk and regulated ecommerce businesses, including supplement brands, nutraceutical merchants, telehealth companies, and subscription operators. Our acquiring relationships and gateway configurations are built with compliance requirements in mind, covering PCI alignment, chargeback mitigation, and fraud prevention tools that support the controls your audit requires.

If your current payment setup cannot withstand a structured infrastructure risk assessment, or if you are building toward one, Davincipay can help you get the right acquiring structure in place. Merchants in regulated categories can review our payment solutions or go directly to start your application to connect with our team.

FAQ

What is a merchant payment infrastructure audit?

A merchant payment infrastructure audit is a structured review of your entire payment ecosystem, covering settlement controls, PCI DSS compliance, fee analysis, dispute management, and vendor governance. It goes beyond checkout security to verify every layer of your transaction lifecycle.

Which PCI DSS SAQ type applies to my ecommerce business?

Your SAQ type depends on how your payment pages are built. SAQ A applies to fully outsourced payment pages, SAQ A-EP applies to merchants hosting payment-influencing pages without storing card data, and SAQ D applies to merchants who store cardholder data directly.

How long should audit logs be retained for PCI DSS compliance?

PCI DSS requires audit logs to be retained for at least one year, with a minimum of three months immediately available for forensic analysis and incident reconstruction.

How do I audit payment systems for hidden processor fees?

Review three months of merchant statements and build a spreadsheet separating pass-through interchange fees from processor markups. A forensic statement review typically takes 60–90 minutes and identifies fees labeled as service charges or network access fees that represent pure processor margin.

What vendor evidence do I need for a third-party risk audit?

You need current SOC 2 Type II reports from critical vendors, contract clauses granting audit rights, and documented ongoing monitoring records including incident notifications and performance reviews. A contract right without collected evidence does not satisfy examiner expectations.

.webp)