.png)

Merchant account risk scoring is a numerical assessment that payment processors assign to your business based on transaction data, dispute history, and operational behavior. Processors like Stripe, PayPal, and specialized underwriters use this score to decide whether to approve your account, set your fees, require reserves, or terminate your processing relationship. The score is not a single fixed number. It updates continuously as new data arrives. For ecommerce businesses in high-growth or regulated verticals, understanding how this score works is the difference between stable payment processing and a sudden account freeze.

What is merchant account risk scoring and how is it calculated?

Merchant account risk scoring is the industry term for what underwriters and processors formally call merchant risk assessment. The score reflects the probability that your account will generate financial losses through chargebacks, fraud, or insolvency. Processors calculate it using a blend of transaction and operational data, updated continuously as your business processes payments.

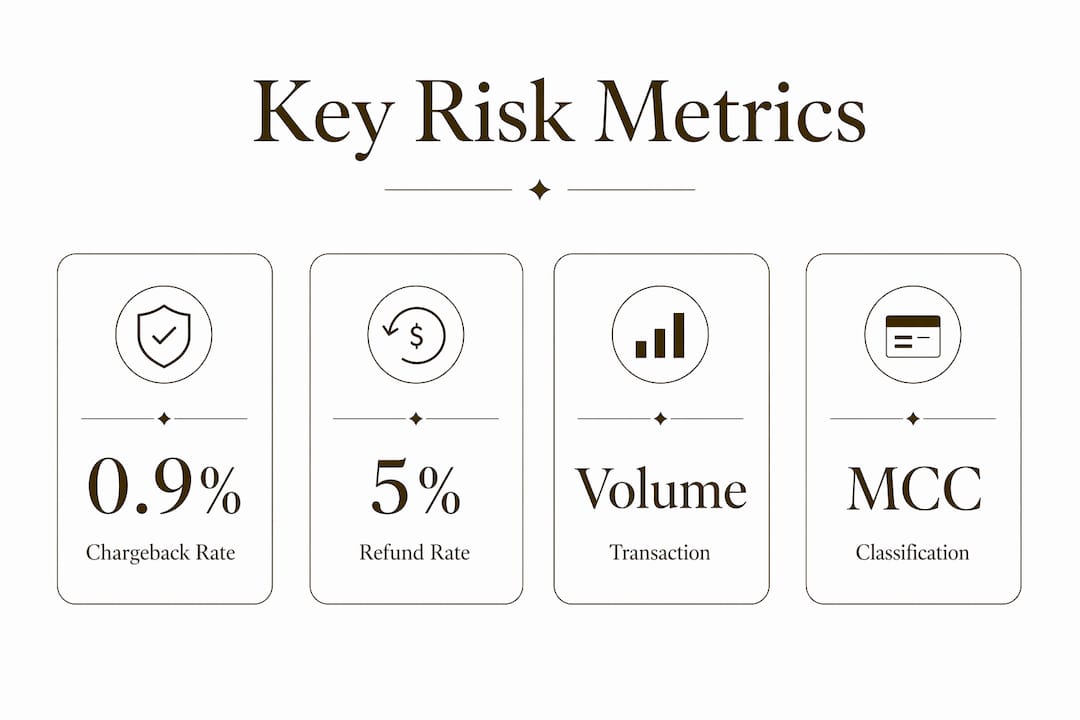

The most influential input is your chargeback rate. Processors flag accounts above roughly 0.9%, and Visa’s VAMP program begins monitoring at 0.5%, with elevated scrutiny at 0.9%. Exceeding these thresholds triggers fines, remediation requirements, or account termination. That means a single bad month can move your account from standard to high-risk status.

Refund rates carry nearly as much weight. Refunds above 5% raise concern, and rates above 10% are treated as red flags. Refunds matter because they predict future chargebacks before those disputes formally appear on your record.

The table below summarizes the main metrics processors use and what each one signals.

MetricRisk SignalThreshold to WatchChargeback rateDispute frequency and fraud exposureAbove 0.9% triggers scrutinyRefund rateEarly indicator of customer dissatisfactionAbove 5% raises concern; above 10% is a red flagTransaction volumeRevenue consistency and operational stabilitySudden spikes or drops raise flagsAccount ageBusiness maturity and track recordNewer accounts carry higher baseline riskCustomer retentionRepeat purchase patterns and trust signalsLow retention suggests product or fulfillment issues

Pro Tip: Track your chargeback and refund rates weekly, not monthly. By the time a monthly report shows a problem, your processor may have already flagged your account.

How does risk scoring impact your payment processing?

A high merchant risk score produces real, immediate consequences for your business. Elevated risk scoring triggers higher processing fees, rolling reserves, volume caps, or full account termination. These outcomes are not arbitrary. They follow defined thresholds that processors apply consistently.

Processors do not share your numeric score with you. You infer it from what happens to your account. Common signals include:

The most severe outcome is placement on the MATCH list, maintained by Mastercard. A MATCH listing follows you for five years and makes it extremely difficult to open a new merchant account anywhere. Processors check this list during underwriting, and a listing is often disqualifying on its own.

Pro Tip: If your processor suddenly requests updated bank statements or business documentation, treat it as a risk review in progress. Respond quickly and completely. Delays signal instability.

High-risk banking solutions exist specifically for merchants who have been flagged or terminated. Understanding fee and reserve structures before you sign a processing agreement helps you avoid surprises later.

How do underwriters evaluate risk beyond the score?

The numeric score is one input in a broader merchant risk assessment process. Underwriters weigh several additional factors when making final decisions about approval, reserves, and volume limits. Underwriters consider business model fit, transaction consistency, dispute velocity, and operational transparency during both onboarding and periodic reviews.

The key factors underwriters examine beyond the score include:

Underwriting outcomes fall into four categories: full approval, approval with a rolling reserve, approval with volume limits, or denial. Each outcome reflects where your risk profile sits relative to the processor’s internal thresholds.

What steps can you take to improve your merchant risk score?

Managing your merchant account risk evaluation is an ongoing process, not a one-time fix. The goal is to keep every key metric comfortably below processor thresholds so that normal business fluctuations do not trigger a review. Here is a practical sequence to follow:

Pro Tip: Use a dedicated chargeback management tool like Chargebacks911 or Midigator to track dispute patterns in real time. Catching a dispute trend early gives you time to fix the underlying cause before your processor notices.

Operational controls like refund workflows, dispute evidence libraries, and proper MCC classification stabilize your risk metrics over time. Small metric changes near thresholds cause outsized consequences. Staying well below those thresholds is the most reliable protection you have.

Key takeaways

Merchant account risk scoring is a dynamic, continuously updated assessment that directly controls your processing fees, reserves, and account stability.

PointDetailsChargeback rate is the top metricKeep your rate below 0.5% to avoid Visa VAMP monitoring and processor scrutiny.Refunds predict future chargebacksA refund rate above 5% signals elevated risk before disputes formally appear.Scores are internal but visibleInfer your risk status from fund holds, fee changes, reserve requirements, and volume caps.Underwriting goes beyond the scoreMCC classification, website compliance, and revenue consistency all affect underwriting outcomes.Consistency builds credibilityA long, clean processing history carries more weight than short-term perfect metrics.

The part most merchants get wrong about risk scores

Most merchants I work with assume their risk score is a fixed grade, something assigned at onboarding and reviewed once a year. That assumption is expensive. Risk scoring is continuous, and your score can shift meaningfully within a single billing cycle.

The merchants who get into trouble are almost never the ones with obviously bad practices. They are the ones operating just below a threshold, running a promotion that spikes volume, or launching a new product with a higher return rate. One month of elevated refunds moves them from “standard” to “under review” with no warning.

What I tell every ecommerce operator is this: your risk score is a reflection of your customer experience. A poor checkout flow, a confusing subscription cancellation process, or a slow refund turnaround all show up in your dispute data before they show up anywhere else. Fix the customer experience first, and the metrics follow.

The other mistake I see constantly is treating processor communication as adversarial. When a processor asks for documentation, merchants often delay or push back. That response reads as instability. Processors want to keep good merchants. Responding fast and completely to any request signals that you run a professional operation. That signal matters more than people realize.

How Davincipay helps you manage merchant risk

Davincipay works specifically with ecommerce merchants who face complex risk profiles, including nutraceutical brands, supplement businesses, telehealth companies, and subscription merchants. We understand that a single risk flag can disrupt your entire revenue operation.

Davincipay connects you with domestic and international acquiring relationships built for high-risk verticals. Our underwriting support helps you enter the right risk tier from day one, and our chargeback mitigation tools keep your metrics where they need to be. If you are ready to secure stable payment processing with a team that understands your risk environment, apply now and get a fast approval decision tailored to your business.

FAQ

What is merchant account risk scoring?

Merchant account risk scoring is a numerical assessment that payment processors use to evaluate the financial and operational risk associated with a merchant account. It is calculated from chargeback rates, refund rates, transaction volume, account age, and revenue consistency.

Do processors share your risk score with you?

Processors do not disclose your numeric risk score directly. You can infer your risk status from account restrictions, rolling reserves, fee increases, or sudden fund holds on your account.

What chargeback rate triggers a risk review?

Visa’s VAMP program begins monitoring at a 0.9% chargeback rate, with elevated scrutiny applied above that level. Most processors flag accounts internally before they reach the formal network threshold.

How do i lower my merchant risk score?

Monitor chargeback and refund rates weekly, maintain consistent transaction volume, verify your MCC classification, and keep your website fully compliant with clear refund and cancellation policies.

What happens if my risk score gets too high?

A high risk score leads to higher processing fees, rolling reserves, volume caps, or account termination. The most severe outcome is placement on the Mastercard MATCH list, which restricts your ability to open new merchant accounts for five years.

.webp)