.png)

Finding a high-risk payment processor that actually approves your business fast without exposing you to costly account freezes is harder than it should be. Many providers gate their rates and requirements behind sales calls or only give you multi-week onboarding with no guarantee of approval. This comparison gives you details on speed, compliance, and industry acceptance across five Easy Pay Direct alternatives so you can choose a processor that solves urgent onboarding without hidden hoops.

Table of contents

Davincipay

At a glance

DavinciPay’s marketing materials state approvals can occur within 24 hours for some high-risk applicants. The vendor advertises PCI Level 1 payment handling as part of its security posture. The company emphasizes real-time dashboards, chargeback support, and onboarding aimed at getting merchants processing quickly.

Core features

Key differentiator

The claim above about approvals in 24 hours is the focal capability. DavinciPay pairs that speed with tailored risk assessment designed for high-risk verticals. That combination aims to reduce the time between underwriting and live processing for merchants refused by legacy processors. The emphasis is on getting accounts live fast while keeping compliance documentation in place.

Pros

Cons

Who it’s for

DavinciPay fits high-risk merchants who need a provider willing to accept categories other processors avoid. Typical users include nutraceutical brands, telehealth practices, subscription merchants, and CBD or hemp sellers. Choose this if fast onboarding, underwriting support, and chargeback handling matter to your cash flow.

Unique value proposition

Domestic and international acquiring relationships combined with underwriting and chargeback mitigation let you place accounts where underwriters will accept risk. That setup aims to reduce account churn and open processing lanes for regulated products. For teams that lose revenue to frequent processor rejections, this model can restore sales continuity.

Real world use case

According to the company, a telehealth startup secured payment processing that supports HIPAA compliance, recurring billing, and chargeback management. The vendor says that setup helped the startup recover lost authorization rates and maintain subscription billing. The example aligns with the platform’s focus on regulated online services.

Pricing

Pricing is not published on the site. The product data lists the offering as informational only and notes missing detail pages. Contact sales or a DavinciPay representative for custom quotes and rate schedules.

Website: https://davincipay.ai

PayDiverse high-risk payment processing

At a glance

PayDiverse’s marketing materials claim 24–48 hour payouts to merchants. That promise targets sellers who need faster cash flow than typical providers offer. According to the company, it also brings over 20 years of experience and multiple domestic and international banking partners.

Core features

Core payment and risk controls cover the main needs of high-risk merchants.

Key differentiator

PayDiverse’s marketing materials state it maintains the largest network of specialized high-risk banks and offshore solutions. That network supports multi-bank routing to reduce single-bank exposure for volatile accounts. The vendor positions these banking relationships as the core way it manages high-risk portfolios. This focus suits merchants who need alternatives to standard acquirers.

Pros

Cons

When it may not fit

PayDiverse is not a fit for low-risk merchants seeking the cheapest possible processing. Businesses with straightforward retail profiles will likely find lower rates elsewhere. Merchants who cannot supply thorough underwriting documentation should expect longer reviews and possible declines.

Who it’s for

This product fits high-risk merchants who need alternative acquiring relationships and faster payouts. Typical users include CBD sellers, supplement merchants, travel operators, and coaches with high-ticket offers. Choose this if prior processors have declined your business or if multinational routing is a priority.

Real world use case

A CBD oil supplier with recurring chargebacks used PayDiverse to open a merchant account with offshore options. The supplier moved large international orders through multiple acquiring paths. That setup reduced single-bank exposure and kept processing active during a high-volume sales period.

Pricing

Pricing is not explicitly specified in public materials. PayDiverse uses custom pricing based on industry and risk profile. Expect to provide detailed business documents to receive a tailored rate and fee schedule.

Website: https://paydiverse.com

Instabill

At a glance

Instabill reports support for over 160 currencies, a notable claim for merchants selling across many countries. The company traces its roots to 2001 and focuses on both high risk and low risk merchant accounts for e-commerce, retail, and MOTO businesses. It emphasizes live customer support and customized setups for complex merchant profiles.

Core features

Instabill centers on merchant account provisioning, payment routing, fraud controls, and international banking relationships. Key capabilities include:

These features align with needs of merchants who process cross-border volume or operate in regulated verticals.

Key differentiator

Instabill focuses on high risk merchant accounts supported by a network of domestic, offshore, and international banking partners. That network is its main edge when your business cannot get conventional acquiring. The vendor frames its service as adaptable to complex underwriting requirements and custom account structures.

Pros

- Fast approvals and onboarding that reduce processing downtime for new merchant accounts.

- Transparent interchange plus pricing with volume discounts. Specific rates are supplied after application and underwriting.

- Tailored underwriting and support for high risk and regulated industries, which lowers account closure risk.

- Integrated fraud screening plus dispute management to cut manual chargeback effort.

- Global processing with local acquiring partners helps merchants expand into new countries.

Cons

- Public pricing detail is limited; you must apply to see concrete rates and fee structures.

- The product focuses on specialized and high risk verticals, so very small or purely domestic sellers may find it excessive.

- Vendor and buyer comments highlight account longevity claims, but independent third party verification is sparse.

When it may not fit

If you need a standardized, self-serve pricing model, Instabill may not match your expectations. Shops that require plug-and-play integrations with specific platforms should verify support first. Businesses with very low risk profiles and simple acquiring needs may find the setup and underwriting overhead unnecessary.

Who it’s for

Instabill fits merchants that operate in high risk verticals or that need international acquiring options. Choose it if your business requires customized underwriting, offshore settlement, or live support during onboarding. It also suits retail operations that need POS plus gateway combined with multi-currency routing.

Real world use case

A startup CBD store used Instabill to get a merchant account that accepts international cards and settles in multiple currencies. The store required PCI compliance, fraud screening, and a banking partner willing to support its vertical. Instabill handled underwriting and provided a payment gateway plus ongoing support during scaling.

Pricing

Instabill does not publish standard rates in the provided material. Pricing typically varies by industry, transaction volume, and perceived risk level. Plan for custom quotes and documentation-driven underwriting during rate negotiation.

Website: https://instabill.com

Durango merchant services

At a glance

Durango assigns a dedicated account manager to most merchants for onboarding and account recovery support. That hands-on model targets merchants in high risk and large volume retail niches. The company pairs multi currency card acceptance with fraud protection and tailored gateway setups. These elements aim to keep processing stable during rapid growth.

Core features

Durango offers fast approvals for merchant accounts and dedicated account managers who handle underwriting and recovery. The platform supports credit card processing, ACH, and echeck along with mobile wallets such as Apple Pay and Google Pay. According to the company, Durango supports over 150 shopping cart platforms. Pricing is billed interchange-plus, and merchants can request custom, industry-specific gateways.

Key differentiator

Durango focuses on industry specific, customizable merchant gateways plus personal account management. That combination suits merchants who need a payment setup built around their product, compliance needs, and sales flows. The vendor also advertises account recovery services for merchants previously frozen or closed by major processors.

Pros

Cons

When it may not fit

If you run a low-risk small business with simple processing needs, Durango may be overqualified and costlier than mainstream processors. If you need immediate, published rate tables, the lack of public pricing creates extra friction. If your company operates in an unsupported country, you will need an alternate acquirer.

Notable integrations

Who it’s for

Durango fits merchants in high risk industries or retail businesses with high transaction volume. Choose it if you need tailored underwriting, gateway customization, or a named account manager. It also suits teams expanding internationally who require multi currency acceptance.

Real world use case

A telemedicine platform used Durango to obtain a high risk merchant account while launching abroad. The setup accepted multiple currencies and routed payments through an industry specific gateway. The account manager handled underwriting and helped prevent processing interruptions during rapid user growth.

Pricing

Durango uses transparent interchange-plus pricing, but exact rates depend on industry, volume, and risk profile. Prospective merchants must contact sales for a custom quote and contract terms.

Website: https://durangomerchantservices.com

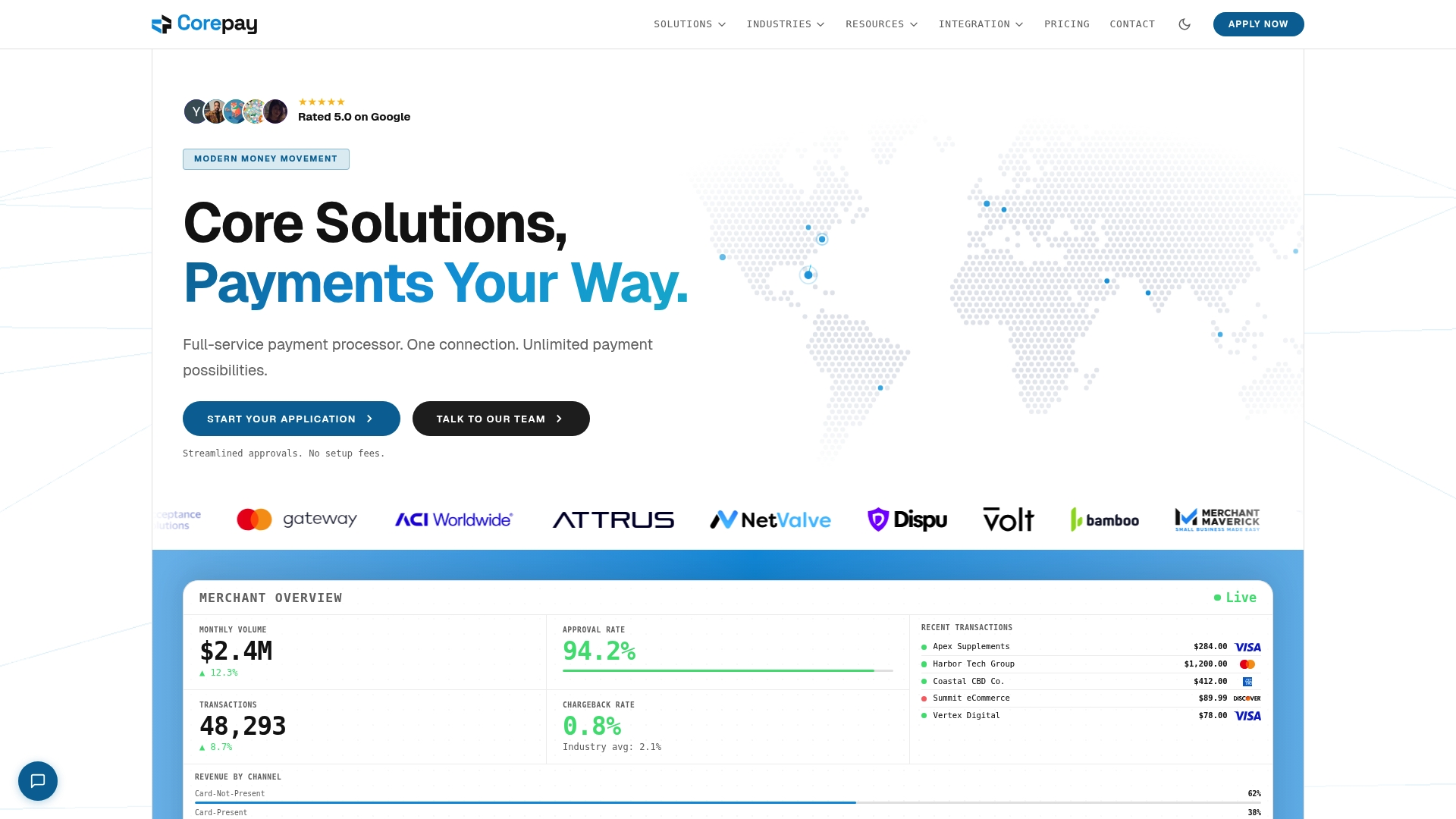

Corepay

At a glance

Corepay’s marketing materials state it processes payments in over 135 currencies across 30+ countries. The company pairs direct acquiring relationships with payment routing, fraud screening, and industry underwriting. Corepay targets merchants rejected by mainstream processors and focuses on regulated verticals like healthcare and telehealth.

Core features

Corepay delivers full service payment processing through direct acquiring partners in major markets. Their payment orchestration routes transactions to improve approval rates and reduce declines. Recurring billing handles subscriptions with automated retry logic for failed charges. Real time fraud screening links to chargeback management to lower dispute overhead. Multi region processing manages local compliance across the United States, European Union, United Kingdom, and Australia.

Key differentiator

Corepay underwrites complex verticals internally and issues merchant accounts designed for long term stability. That internal underwriting reduces the chance of sudden account closures common with general purpose processors. The combination of underwriting and local acquirers supports sustained processing for healthcare, telehealth, and other regulated merchants.

Pros

Cons

When it may not fit

Corepay fits merchants that need tailored underwriting and global acquiring for regulated activity. It may not fit low risk, very small volume shops that only need basic domestic processing. Also avoid Corepay if you require fixed public rate cards because pricing requires application and custom quoting.

Notable integrations

Who it’s for

This product suits merchants in healthcare, telehealth, online pharmacy, and high risk ecommerce looking for tailored payment infrastructure. Choose Corepay if you need underwriting that matches regulated workflows and multi currency acceptance. It matches teams that require long term account stability and regional acquiring relationships.

Real world use case

A telehealth clinic operating across several states needed HIPAA data separation, recurring billing, and multi state licensing support. Corepay provided underwriting that supported the clinic’s billing patterns and reduced the risk of account suspension from generic processors. The clinic kept subscription revenue flowing while meeting compliance needs.

Pricing

Corepay uses interchange plus pricing with volume discounts and custom fees based on risk and volume. Specific rates, monthly fees, and discount tiers are provided only after application and underwriting.

Website: https://corepay.net

Comparison of alternatives

Choosing a reliable payment processing solution is imperative for high-risk merchants aiming to achieve efficient operation in regulated industries. Different providers bring unique advantages, from fast approval workflows to specialized support for international operations and compliance.

Approval timelines

DavinciPay stands out in offering expedited processing approvals, advertising timelines as short as 24 hours for certain high-risk merchants. This capability enables potential revenue stabilization faster than competitors like Instabill, whose underwriting complexity extends required timeframes. For businesses prioritizing high-speed entry into operational capability, this factor notably benefits DavinciPay users.

Banking coverage and international handling

Where banking network coverage is critical, PayDiverse excels through its partnerships with numerous high-risk and offshore banks. This combination facilitates diverse account setups, accommodating international revenue streams effectively. While DavinciPay also emphasizes international compatibility, PayDiverse’s multipath acquisition solutions cater particularly well to businesses with global ambitions.

Best fit

Our pick

DavinciPay remains the most effective choice when high-risk merchants need rapid application approval and a secure, tailored onboarding solution. Its capacity to serve challenging sectors swiftly and reliably surpasses competitors for businesses prioritizing these specific attributes.

When considering high-risk payment processors, it is crucial to evaluate each platform’s unique features and benefits while weighing their pricing transparency and suitability for your industry.

ProductKey DifferentiatorBest ForPricingNotable LimitationDavincipayTailored, rapid approval for high-risk industriesHigh-risk merchants in regulated verticalsNot disclosedLimited pricing transparency publicly availablePayDiverseExtensive network of high-risk banksMultinational merchants with offshore needsNot disclosedVariable outcomes with third-party approvalsInstabillSupport for over 160 currenciesMulti-industry international merchantsNot disclosedRequires extensive documentation for onboardingDurango Merchant ServicesDedicated account management for onboardingHigh-volume and specific industry merchantsNot disclosedStringent vetting for some industriesCorepayIntegrated fraud screening and global acquiringHealthcare-focused high-risk merchantsNot disclosedFocuses on specific verticals; limited fit for very small sellers

Find a reliable Easypaydirect.com alternative with Davincipay

Struggling to find a payment partner that truly supports high-risk and regulated ecommerce? Many merchants face hurdles like slow approvals, frequent account closures, and incomplete chargeback support when searching for easypaydirect.com alternatives. Davincipay specializes in fast approvals tailored for complex businesses including nutraceutical brands, telehealth firms, and subscription services. We combine domestic and international acquiring relationships with strong underwriting and fraud prevention to keep your processing secure and uninterrupted.

Key benefits include:

Don’t let payment roadblocks stall your growth. Visit Davincipay today and book a consultation to secure your merchant account in 24 hours or less.

FAQ

What are the approval times for Davincipay compared to other platforms?

Davincipay can process approvals within 24 hours for some high-risk applicants, which is faster than many traditional processors. The platform emphasizes rapid onboarding tailored for high-risk merchants, making it an excellent choice if you need quick access to payment processing.

How does Davincipay handle chargeback management compared to PayDiverse?

PayDiverse provides dedicated fraud prevention tools and chargeback alerts, which are strong features for managing disputes. In contrast, Davincipay focuses on ongoing underwriting support alongside chargeback management to help keep merchant accounts active, particularly beneficial for high-risk industries.

Can businesses with high transaction volumes rely on Davincipay?

Yes, Davincipay supports high transaction volumes, especially for specialized high-risk industries, through tailored risk assessment processes. This feature positions it as a reliable alternative for merchants who have had difficulties with traditional processors.

What is the pricing structure for Davincipay?

Pricing for Davincipay is not available publicly, requiring potential users to contact sales for custom quotes. This lack of transparency can make it a bit challenging during initial evaluation but allows for tailored options based on specific business needs.

Does Davincipay support recurring billing like other competitors?

Yes, Davincipay offers flexible checkout options including subscriptions and recurring payment models, making it suitable for businesses that rely on consistent revenue streams. This feature is vital for high-risk merchants in sectors like telehealth and e-commerce.

.webp)